Paper NACH – The Offline to Online Challenge

Change is always hard. Even more so when it’s for something that’s been done without question for many many years. It is not so much the process that acts as a hindrance as it is the willingness to alter the process. A similar stumbling block came our way while trying to build a product to support Physical NACH or Paper NACH payments.

When we started discussing the viability of creating a Paper NACH product (I know that I have still not elaborated on what this Paper NACH is, but bear with me for just a bit), the business case was very straightforward. More than 80% of the mutual fund and lending sector continues to use Paper NACH to set up recurring payments. Furthermore, we had received multiple asks from our key enterprise clients to build a solution for them. What was less clear was how we wanted to approach this product.

For a user to switch from an existing product to a new one, there need to be substantial gains – a commonly used framework is that the customer’s experience must increase 10x for the switching costs to be justified. Well then the solution was simple really – solve a key pain-point, or many such pain points for that matter, which can help NACH users. However, the key question remained, how do you improve a 2-decade old product?

The Old Way

To understand how we went about solving this I need to first elaborate on the end-to-end NACH mandate process which exists today.

Q: What is a NACH Mandate?

A: A NACH Mandate is an authorization (or permission) that customers provide to Institutions/Businesses to Credit or Debit funds, especially on a recurring basis.

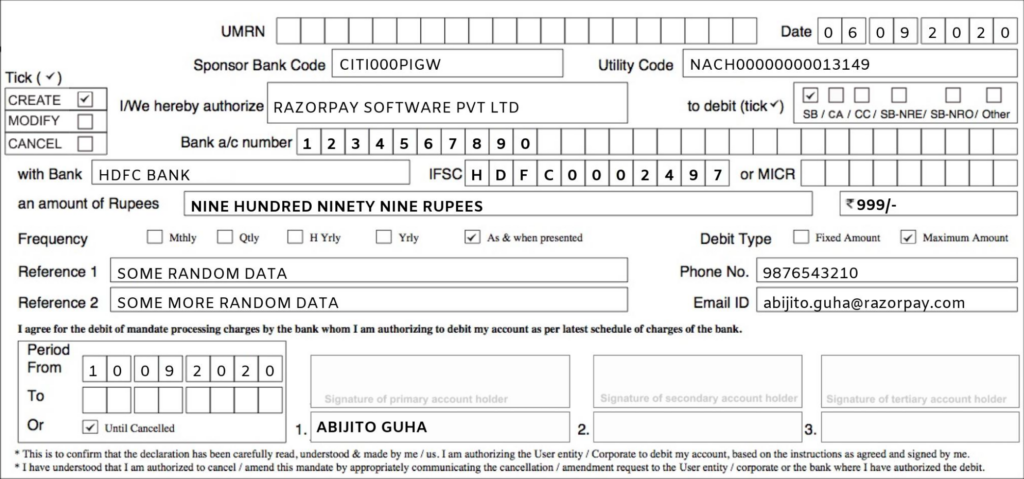

The authorization is provided in the form of a signature by the customer on a piece of paper that has a whole host of other details (see the picture below). This form is then validated by the customer’s bank and the mandate is registered if the necessary conditions are met. Although used widely, this is just like any other bank form that we hurriedly sign and have no clue about what it does.

Not too complicated so far, eh? Well, this is where things get a little `messed up`.

Let’s take the example of setting up an investment. Commonly, the actors involved here would be the customer, the business (firm offering the investment option), and a financial advisor or agent who would be the goto between the customer and the business. The steps involved (after the customer has agreed in principle to buy the product) in setting up the NACH mandate which can be deducted periodically would look something like this:

- The agent fixes up a meeting with the customer to get their documents along with the signature on the NACH form (TAT: 2-4 days)

- The agent submits the NACH form at the local office/branch from where it is couriered to the head office (TAT: 2-4 days)

- Certain firms enlist the help of third parties to collect the documents in which case the TAT may increase

- The Ops team at the head office does a basic check on the NACH form and accepts/rejects it (TAT: 1-2 days. If rejected, the process goes back to Step 1)

- The Ops team then couriers the NACH forms to their payment service provider or PSP (TAT: 2-4 days)

- The PSP receives the NACH forms and proceeds for manual verification of every form (TAT: 1-2 days)

- The PSP submits a softcopy of the NACH form to their sponsor bank and it is finally routed to the customer’s bank for verification (TAT: upto 10 days. If rejected, goes back to Step 1)

While breaking down the above process, it became increasingly evident that the time taken was extensive. Even when everything went smoothly and the NACH form was accepted on the first attempt, the registration process took between 10 – 22 working days i.e. anywhere between 2 weeks to 6 weeks!!! Coupled with the additional costs incurred on agents, mailing/couriering of forms, and the salaries of Ops personnel, this is not only a time-consuming process but also an expensive one.

Add to this the hassle of keeping track of the forms across the registration lifecycle, ensuring that the forms are mapped to the correct customers, and the uncertainty of whether the signature of the customer would match that present in their records with the bank meant that there were enough headaches to go around.

Identifying the Problems with Paper NACH today

Having broken down the process and after identifying the key pain points faced by merchants, the difficult part was on how to go about solving them. Broadly, these were the issues that businesses go through daily:

| Problem | Impact | Solvable |

| Delivery of the NACH forms to the customer | TAT, Cost to company | Yes |

| Customer to sign the NACH form | TAT | No |

| Delivery of NACH form to the team which verifies the data | TAT, Cost to company | Yes |

| Verification of NACH form (while meeting the industry standards on accuracy) | TAT, Cost to company | Yes |

| Submission of form to the PSP | TAT, Cost to company | Yes |

| Processing time taken to approve/reject the mandate by the customer’s bank | TAT | No |

Any problem, however complex, seems less daunting once it is broken up into smaller problems; parts that can be solved. The behemoth that is the NACH mandate also seemed less of a Goliath once we were able to break it down.

Obviously, there were parts that were outside of our control, namely the customer signing the NACH form and the time taken by the destination bank to approve the mandate.

On the first, well duh! Let’s be honest – a customer signs a form when it is convenient to him/her and not a second sooner (also, speaking from personal experience – I can never keep my signature consistent, and it looks different every time!). It didn’t really make sense to lose sleep pondering over this. The second one, i.e the time taken by the destination bank to approve the mandate was again outside of our hands. Once the form is submitted, every bank and branch has its own process – and solving this for lakhs of bank branches across over 1300 member banks on the NACH platform was again a non-starter.

The others, however, could be solved. Maybe.

The Switch to Online

The `solvable` problems could be further classified into 2 buckets:

- Steps involving the delivery of the form across multiple stakeholders

- Verification of the data on the form

The delivery problem was something Razorpay was already good at. Businesses using Razorpay’s other recurring products already have the option of sending payment links directly to customers via email, WhatsApp, and SMS, to make a payment. It seemed all the more apt here since businesses could save on additional costs by sharing the NACH form directly with the customer as any other payment link. What we additionally provided was the ability to generate a prefilled NACH form on which the customer simply had to sign. This could be done by either using our powerful REST APIs or from the merchant dashboard.

Once the customer signed the form, the problem of delivering the form to the agent who in turn delivers the form to the local office could also be solved by simply asking the customer to submit a photo of the form on the payment link itself. Thus from a customer’s perspective, it was just the case of receiving a link, downloading and signing the form from the link, and uploading a photo of the signed form onto the same link. To simplify the experience, we designed the process similar to that of uploading an image on WhatsApp. This completely removed the dependency on agents and other human touchpoints.

The delivery alone would not solve everything, sadly. Else everyone would’ve done it. The industry norm was for every form to be manually verified before being submitted for approval to the bank. This was another time-consuming and expensive process. To tackle this, we put in place an Optical Character Recognition (OCR) engine to read the form. An OCR is a tool that uses Machine Learning algorithms to identify the text on a form. In our case, we used the OCR to read the data on the form which was being submitted by the customer and let them know in real-time whether the form submission was successful or not. If the event of an error, the customer immediately gets to know what the issue is and can take corrective measures.

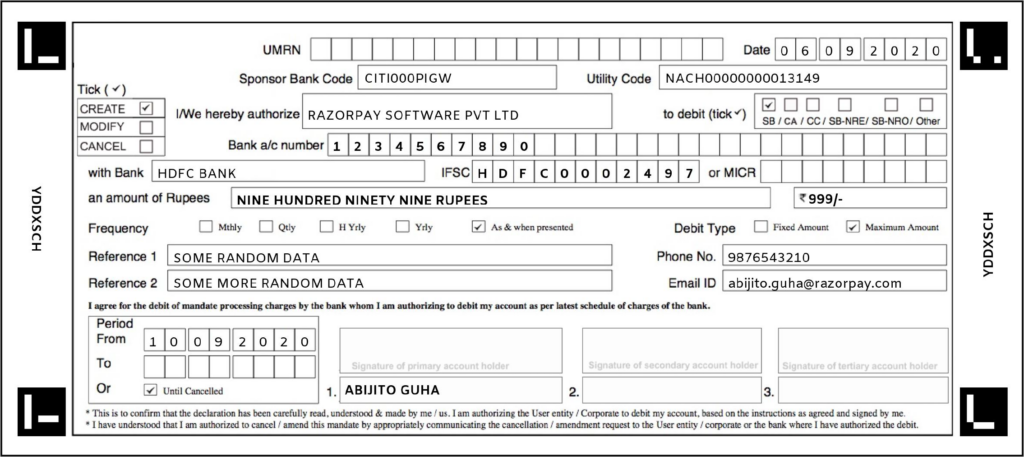

The below image is an illustration of the form used at Razorpay. The black boxes on the sides help the OCR engine identify the text, even in the case of a slight crumpling of the form. The rest of the form is as per the existing NPCI-mandated design. As an added measure of security, every form is also generated with a unique security code to ensure that the correct form is uploaded and to prevent tampering.

We launched our Paper NACH product in February of 2020 to a select set of businesses as part of an initial pilot. Of course, we had no idea of what was going to happen, and when the Covid outbreak and the subsequent lockdown came upon us, the Paper NACH product was one of those which had to take a back seat for obvious reasons. But, as everyday life begins to slowly recover towards some semblance of normalcy, we were mildly surprised to see businesses warm up to our offering. What has proven particularly attractive is the drastic cut down in the human touchpoints. Working at reduced capacities, the option of eliminating the agent or middle man and to be able to bypass the Ops process has helped over 30 businesses continue using Paper NACH for their day-to-day work, thus making the pilot a success.

As we progress to the next phase of the product journey, it’s important to note that we at Razorpay haven’t broken the wheel. The process for NACH mandates remains the same. However, what we have done is to try to improve and optimize wherever possible. The TAT for form submission, before it reaches the destination bank, can be just a few hours as opposed to taking days or even weeks in the offline system. The costs incurred by businesses using our services have also substantially reduced. All it took was a little change.