- The Ultimate Guide for Businesses")

The way Indian consumers transact is undergoing a significant evolution, and at the forefront of this shift is the burgeoning “Buy Now, Pay Later” (BNPL) ecosystem. Projected to reach a staggering $21.95 billion in 2025, with an anticipated climb to $35.07 billion by 2030, Buy Now, Pay Later is no longer a niche offering but a rapidly solidifying payment preference. This surge, fueled by a 27% growth in India’s e-commerce sector in 2023 and a credit card penetration rate hovering around a mere 5%, highlights a clear demand for accessible and flexible payment solutions. For businesses navigating this dynamic landscape, understanding and strategically implementing BNPL isn’t just about keeping pace; it’s about unlocking new avenues for growth, enhancing customer acquisition, and optimizing the very pulse of online transactions – the checkout process. This guide delves into the intricacies of BNPL for Indian businesses, offering a comprehensive understanding of its benefits, risks, regulatory nuances, and practical steps for seamless integration.

What Exactly is Buy Now, Pay Later (BNPL) and How Does it Work for Your Customers?

At its core, Buy Now, Pay Later offers your customers an alternative to traditional payment methods by splitting the cost of their purchases into a series of smaller installments over a defined period. BNPL is typically offered at the point of sale, most commonly during the checkout process on your website, and allows shoppers to receive their goods or services immediately while deferring the full payment.

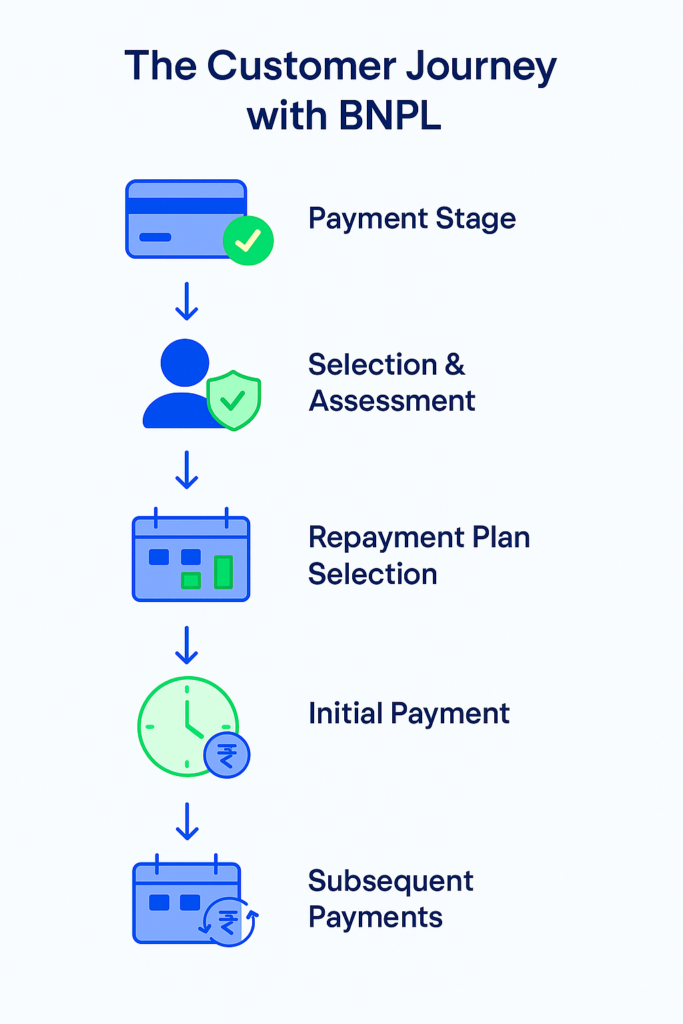

The Customer Journey with BNPL:

The Customer Journey with BNPL:

Payment Stage: During the checkout process, customers see BNPL as a payment option.

Selection & Assessment:

- Customer selects the Buy Now, Pay Later option.

- They are typically redirected to the Buy Now, Pay Later provider’s interface.

- A quick, automated assessment takes place, often involving providing personal details.

- A “soft” credit check, which usually doesn’t impact their credit score, might be conducted.

Repayment Plan Selection: If approved, customers choose from available repayment plans:

- Interest-free installments: Spread over weeks or months, where the total purchase price is divided into equal payments.

- Longer-term options: May include interest charges.

Initial Payment:

- Not always mandatory: Many Buy Now, Pay Later options, especially short-term, interest-free plans, do not require an immediate upfront payment. The first installment is often scheduled for a later date.

- Sometimes required: Some providers or plans, particularly for higher-value items or longer terms, might require a down payment at the time of purchase.

Subsequent Payments: The remaining balance (or the entire amount if no initial payment was made) is automatically debited from the customer’s linked payment method (debit card, credit card, or UPI) based on the agreed repayment schedule.

The appeal for your customers lies in its perceived affordability and flexibility, allowing them to manage their budgets more effectively without the immediate financial outlay of the total purchase price. Understanding this process from your customer’s perspective is crucial for effectively integrating and promoting Buy Now, Pay Later on your platform.

Key Benefits of Offering BNPL to Your Customers

Integrating Buy Now, Pay Later into your payment options can unlock a multitude of benefits that directly impact your bottom line and customer relationships:

- Increased Sales and Conversion Rates: By lowering the immediate financial barrier, Buy Now, Pay Later encourages hesitant shoppers to complete purchases, especially for higher-value items. Merchants offering BNPL can experience a 10-30% uplift in sales conversion.

- Higher Average Order Value (AOV): The ability to spread payments makes larger purchases more manageable, prompting customers to add more items or opt for premium versions, boosting your overall revenue.

- Attracting New Customer Segments: Buy Now, Pay Later appeals to younger demographics and those preferring flexible payment solutions over traditional credit, allowing you to expand your customer base.

- Improved Customer Loyalty and Repeat Purchases: Providing a convenient and customer-centric payment option enhances the shopping experience, fostering goodwill and increasing the likelihood of repeat business.

- Potentially Reduced Risk of Chargebacks: In certain Buy Now, Pay Later models, the provider assumes the risk of chargebacks, offering an added layer of financial security for your business.

- Powerful Marketing Tool: Strategically promoting your BNPL offering can attract customers actively seeking flexible payment options and differentiate you from competitors.

To offer BNPL, EMI, and more affordability solutions on your website, explore Razorpay’s Affordability Suite.

BNPL vs EMI: What’s Better for Consumers and Businesses?

As BNPL gains traction, it’s often compared to traditional Equated Monthly Installments (EMIs), a popular affordability option that Indian consumers have long used. While both enable deferred payments, the two work differently and serve distinct customer needs.

Here’s a practical breakdown:

| Criteria | BNPL | EMI |

| Onboarding | Instant, minimal KYC, often no documentation | Requires full KYC, credit approval |

| Credit Check | Usually soft check or none | Hard credit check, affects credit score |

| Tenure | Short-term: 15 days to 3 months (typically interest-free) | Long-term: 3 to 24+ months (often interest-bearing) |

| Interest | Typically 0% for short terms | Usually includes interest or processing fees |

| Ease of Use | One-tap at checkout, seamless for repeat purchases | Requires selection of bank/NBFC plan, more steps |

| Target Audience | First-time credit users, millennials, Gen Z | Credit-savvy users with established credit history |

| Impact on Credit Score | Minimal to none | Regular EMIs build or hurt credit score based on repayment behavior |

So, which is better?

For Consumers:

- BNPL offers instant, low-friction financing and is great for smaller or impulse buys.

- EMIs are better suited for high-ticket purchases needing longer repayment cycles.

For Businesses:

- BNPL can increase conversions and AOV without adding complexity for the buyer.

- EMI attracts credit card holders and enables higher-value sales, but may introduce more checkout drop-offs.

Best Practice: Offer both BNPL for fast, low-ticket purchases and EMI for premium items, and let your customers choose the flexibility they prefer.

Potential Risks and Considerations for Your Business

While the benefits of offering BNPL are compelling, it’s crucial for businesses to also consider the potential risks and operational aspects:

- Transaction Fees: Buy Now, Pay Later providers charge fees on each transaction, which can be higher than traditional credit card processing fees. Carefully evaluate and factor these costs into your pricing.

- Potential for Increased Returns: The ease of BNPL might lead to more impulse buying and, consequently, a higher volume of returns. Implement clear return policies and efficient return management.

- Cash Flow Management: Understand the payout timelines from your Buy Now, Pay Later provider, as it might not be immediate and could impact your cash flow projections.

- Integration Complexity: Assess the ease of integrating Buy Now, Pay Later platforms with your e-commerce infrastructure. Some integrations might require more technical effort than others.

- Potential Impact on Brand Reputation: Customer difficulties with BNPL arrangements or debt could indirectly reflect negatively on your brand.

- Fraud Risks: Be aware of potential fraud associated with BNPL transactions and implement appropriate security measures.

How to Apply for and Integrate BNPL as a Business in India

Implementing BNPL on your e-commerce platform in India typically involves the following steps:

- Research and Selection of a BNPL Provider:

- Identify Popular Providers: Explore prominent BNPL players in the Indian market such as LazyPay, Simpl, ZestMoney, Amazon Pay Later, Flipkart Pay Later, and others.

- Compare Key Factors: Evaluate providers based on:

- Merchant Fees: Understand their transaction charges.

- Integration Ease: Check compatibility and available plugins for your e-commerce platform (e.g., Shopify, WooCommerce, local platforms).

- Customer Reach: Consider their existing user base in India.

- Repayment Terms for Customers: Review the flexibility and options offered to buyers.

- Industry Specialization: Some providers might focus on specific sectors.

- Customer Support: Assess the quality and availability of their support for merchants.

- Application Process:

- Visit Provider Website: Navigate to the merchant or business section of your chosen provider’s website.

- Create a Merchant Account: Sign up and provide your business details.

- Verification: Undergo their verification process, which may involve submitting:

- Business registration documents (e.g., GSTIN).

- KYC documents of the business owners/directors.

- Bank account details.

- Website/app details.

- Agreement: Review and accept their merchant agreement and terms of service.

- Integration with Your E-commerce Platform:

- Check for Direct Plugins/Apps: Many platforms like Shopify, WooCommerce, and others have dedicated plugins or apps for popular Buy Now, Pay Later providers that simplify integration.

- API Integration: If a direct plugin isn’t available, you’ll likely need to use the provider’s API (Application Programming Interface). This requires some technical knowledge or the assistance of a developer. Refer to the provider’s API documentation.

- Testing: Thoroughly test the Buy Now, Pay Later integration in a staging environment before going live to ensure a smooth checkout flow for your customers. Check for correct display of the BNPL option, accurate calculation of installments, and proper order processing.

- Internal Training and Marketing:

- Train Your Team: Ensure your customer service and sales teams are well-versed in how BNPL works, the terms offered, and how to address customer inquiries.

- Promote BNPL: Clearly highlight the availability of BNPL as a payment option on your product pages, during checkout, and in your marketing materials to attract customers.

Pro Tip– Whether you are using a standard checkout flow or a one-click checkout solution like Magic Checkout, we recommend connecting with your checkout provider to check the feasibility of adding Buy Now, Pay Later as a payment option and to ensure a seamless integration process. One-click checkout providers like Magic Checkout often streamline the addition of new payment methods; however, it’s always best to confirm the integration steps with their support team.

If you’re looking to improve the overall checkout experience beyond just BNPL, check out this comprehensive blog on optimizing checkout.

The Regulatory Landscape of BNPL for Businesses in India

The Buy Now, Pay Later sector in India operates within a dynamic regulatory environment shaped by the Reserve Bank of India (RBI). While the RBI is actively focused on mitigating potential risks associated with BNPL, its overarching goal is to foster a robust and inclusive digital payments ecosystem.

It’s crucial to understand that the RBI’s stance isn’t inherently against Buy Now, Pay Later , but rather emphasizes responsible innovation and consumer protection. Several RBI initiatives and guidelines provide context:

RBI’s Vision for Digital Payments: The RBI’s “Payments Vision 2025” document outlines a strategic direction for the evolution of payment systems in India. It promotes digital payments for everyone, everywhere, every time, focusing on safety, security, accessibility, and affordability. Buy Now, Pay Later, by increasing affordability and access to credit for certain segments, aligns with this broader vision.

Regulatory Focus Areas: The RBI’s scrutiny of BNPL primarily centers on:

- Consumer Protection: Ensuring transparency in BNPL agreements, preventing hidden fees, and addressing concerns about over-indebtedness.

- Financial Stability: Monitoring the impact of BNPL on the financial system and promoting responsible lending practices.

Key RBI Directives and Circulars:

The Master Directions on Prepaid Payment Instruments (PPIs) and subsequent clarifications impact how some BNPL providers operate, emphasizing the need for secure and regulated payment instruments.

The Digital Lending Guidelines aim to bring greater transparency and fairness to digital lending practices, which can indirectly benefit BNPL users by ensuring clear loan terms and grievance redressal mechanisms.

Implications for Businesses: Businesses offering Buy Now, Pay Later in India need to navigate this evolving regulatory landscape by:

- Prioritizing transparency in their BNPL offerings to customers.

- Partnering with BNPL providers that adhere to RBI guidelines and prioritize responsible lending.

- Staying informed about upcoming regulatory changes and adapting their practices accordingly.

By understanding the RBI’s broader vision and focusing on compliance and ethical practices, businesses can leverage the benefits of BNPL while contributing to a healthy and sustainable financial ecosystem in India.

BNPL as a Key Tactic for Conversion Rate Optimization in India

Offering BNPL in India isn’t just about providing another payment option; it’s a strategic tactic within your broader conversion rate optimization (CRO) efforts. CRO focuses on maximizing the percentage of website visitors who complete a desired action – in this case, making a purchase. BNPL directly influences several key CRO metrics:

- Conversion Rates: By reducing financial friction, BNPL can significantly increase the percentage of visitors who complete their purchases.

- Average Order Value (AOV): As discussed earlier, BNPL empowers customers to spend more, boosting your AOV.

- Customer Acquisition Cost (CAC): By attracting new customers who might not have purchased otherwise, Buy Now, Pay Later can lower your CAC.

To maximize the impact of BNPL on your conversion rates, it’s essential to treat it as a variable to be tested. Experiment with the placement of BNPL messaging on your product pages and during checkout. Try different call-to-action wording (e.g., “Pay in easy installments,” “Split your purchase”). Analyze the performance of different BNPL providers to see which resonates best with your audience. Remember to track the impact of your BNPL offering on your key CRO metrics to continuously refine your approach.

BNPL FAQs: Everything Businesses in India Need to Know

Here are some of the most common questions businesses in India have when considering offering Buy Now, Pay Later (BNPL):

Q1: What are the merchant fees typically associated with BNPL, and how are they regulated in India?

Ans: Merchant fees vary significantly between Buy Now, Pay Later providers. They are usually a percentage of the transaction value and can range from 2% to 8% or even higher in some cases. While there are no specific RBI regulations that cap or standardize these fees, the RBI emphasizes transparency. You must carefully compare fee structures and negotiate the best possible rates.

Q2: How does BNPL impact my cash flow, and are there any RBI guidelines on payout timelines?

Ans: BNPL providers typically pay merchants upfront (minus the fee) while collecting installments from customers. However, the exact payout timeline varies. Some providers offer next-day settlement, while others might have a few days’ delay. Clarify this with the provider to manage your cash flow. The RBI doesn’t mandate specific payout timelines for Buy Now, Pay Later providers to merchants.

Q3: Is BNPL suitable for all types of businesses in India, considering the regulatory environment?

Ans: BNPL is generally well-suited for e-commerce businesses selling consumer goods. However, its suitability for other sectors might vary. Consider factors like:

- Your target audience’s demographics and preferences.

- The average transaction value of your products.

- The potential impact on your margins.

- Regulatory compliance requirements for your specific industry.

Q4: How do BNPL providers handle customer defaults, and what are the implications for merchants under Indian law?

Ans: Buy Now, Pay Later providers handle customer defaults. However, understand your liability and any recourse you might have. Clarify the provider’s collection practices and how they align with fair debt collection practices in India.

Q5: Will offering BNPL cannibalize my existing payment options, and are there any RBI recommendations on managing this?

Ans: Buy Now, Pay Later can supplement, not replace, existing payment options. Offer a variety of choices to cater to different customer preferences. The RBI doesn’t have specific recommendations on managing payment option cannibalization. Monitor customer behavior and adjust your payment gateway setup accordingly.

Q6: How do I choose the right Buy Now, Pay Later provider for my business in India, considering compliance with local regulations?

Ans: Prioritize providers with a strong reputation, transparent terms, and robust compliance measures. Ensure they adhere to RBI guidelines on digital lending and data privacy.

Q7: What are the specific KYC (Know Your Customer) and AML (Anti-Money Laundering) requirements I need to be aware of as a merchant offering BNPL in India?

Ans: While the primary KYC/AML responsibility lies with the Buy Now, Pay Later provider, you need to have your own robust KYC/AML policies as a business. Ensure that your Buy Now, Pay Later provider’s processes align with these.

The Future of BNPL for E-commerce Businesses in India

The Buy Now, Pay Later market in India is poised for continued expansion, presenting both opportunities and challenges for e-commerce businesses. Market projections indicate significant growth in Buy Now, Pay Later transaction value in the coming years, driven by increasing e-commerce adoption and a growing consumer preference for flexible payment options.

Several key trends are shaping the future of BNPL in India:

- Expansion into New Sectors: BNPL is moving beyond traditional retail and e-commerce, with increasing adoption in sectors like healthcare, education, and travel.

- Increased Competition and Innovation: The entry of new players and the evolving strategies of existing providers are leading to greater innovation in BNPL products and services.

- Focus on Enhanced User Experience: Buy Now, Pay Later providers are prioritizing seamless integration, faster approvals, and personalized payment plans to improve the customer experience.

- Emphasis on Responsible Lending: Growing regulatory scrutiny is pushing the industry towards greater transparency and responsible lending practices, which will be crucial for long-term sustainability.

For e-commerce businesses, staying informed about these trends and adapting their strategies to leverage BNPL effectively will be essential for success in the evolving digital marketplace.

Conclusion

BNPL represents a significant evolution in India’s e-commerce landscape, offering both consumers and businesses new levels of flexibility. For businesses, BNPL presents a powerful opportunity to boost sales, attract new customers, and enhance the checkout experience. However, it’s crucial to weigh these benefits against potential risks, such as transaction fees and the need for careful cash flow management. Furthermore, navigating the evolving regulatory environment in India is essential for long-term success. By embracing responsible practices and staying informed, businesses can effectively leverage BNPL to thrive in the dynamic world of Indian e-commerce.