Every business should comply with the implications of tax deducted at source (TDS) on contractor payments, salary payouts, payment to professionals and much more.

Before we go ahead with understanding those implications – some background about TDS.

Every business is required to deduct tax at source before making any payments to contractors, professionals or employees. Usually, TDS is collected at specified rates and deposited to the government every month. Also, a statement of TDS has to be filed every quarter by deductors.

[Pro Tip: You can make your monthly TDS payments in 30 seconds, completely FREE on our new TDS Payment tool]

Let’s start with how TDS applies to business payments such as contractor payments, payments to professionals, and rental payments. And, how RazorpayX Payroll is simplifying it further for small and medium businesses.

Table of Contents

TDS on contractor payments under section 194C

In India, businesses usually prefer hiring contractors for performing labour-extensive jobs. Businesses find it easy to hire a contractor for specific jobs rather than offering permanent roles to several individuals.

Businesses need to enter into a contract with such contractors. These contracts are made for a particular period and are usually subjected to renewal.

According to the income tax act, here is the list of works where TDS on contractor payments is applicable.

- Advertising services

- Catering services

- Carriage of goods and passengers by any other mode than railways

- Manufacturing and supplying products to consumers using materials provided by consumers

- Broadcasting and telecasting services

- Supply of labour for works contract

Do note that contractors or subcontractors must be residents as per the Income Tax Act.

But that’s not all. There are exceptions for TDS on contractor payments.

- No TDS will be deducted from payments made to a contractor or subcontractor when the amount paid does not exceed Rs 30,000 in a single contract and Rs 1,00,000 in aggregate during a financial year

- Payments made by an individual or a HUF to a resident contractor for personal purposes are not subject to TDS

- TDS is not required for payments made to a contractor engaged in plying, leasing or hiring of goods carriages, provided such contractor provides his PAN to the payer

TDS on professional payments under section 194J

It is very common for businesses to hire professionals like lawyers, CAs, writers or designers, consultants for advisory services or on a freelance basis.

Such businesses need to deduct tax at source under section 194J from payments made to resident professionals at a predetermined rate and deposit it to the government.

Following payments are covered under this section

- Professional fees

- Fees for technical services including consulting fees

- Director’s fees other than salary payments

- Non-compete fees

In case of payments other than the director’s fees, TDS will not be deducted when the payment does not exceed Rs 30,000. There is no such limit for TDS on director’s fees.

For technical services, TDS is deducted at the rate of 2% (not for professional services) and 10% for any other payments. This is valid as of 1st April 2020.

TDS on rent under section 194I

Usually, small businesses and startups are not keen on speeding capital on buying office premises, plant, or machinery. Instead, they rent fixed assets to run their day-to-day operations.

In this context, rent is any amount paid for sub-lease, lease, tenancy, arrangement or agreement for using the following assets.

- Building (inclusive of factory buildings)

- Land

- Land appurtenant to any building (inclusive of factory buildings)

- A plant like an industrial or manufacturing facility

- Equipment like tools, computer systems, networks, other infrastructure required for running a business

- Machinery

- Any furniture or fittings

Such rental payments are subject to 10% TDS provided rent paid or payable exceeds Rs 2.4 lakh in a financial year.

Rate of TDS for business payments

Please note that no surcharge and health & education cess will be added to such tax deduction.

Please note that no surcharge and health & education cess will be added to such tax deduction.

The income tax department has recently revised TDS rates as one of the relief measures during COVID-19 outbreak.

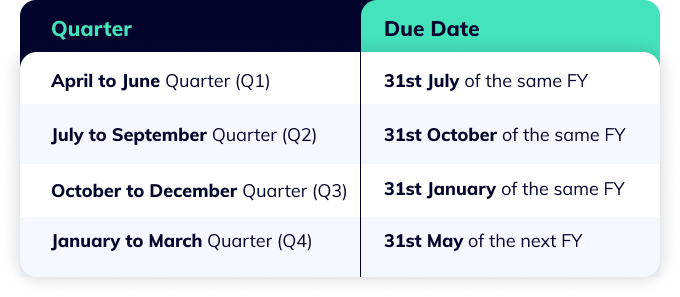

TDS payment due date and return filing

Businesses should deposit TDS to the government within 7 days from the end of the month in which the deduction is made. But, the TDS deducted in March can be deposited on or before 30th April.

Once payments are made, every deductor should file TDS returns reporting all the eligible transactions made during a period to the government. [bctt tweet=”A business needs to file TDS return through Form 26Q every quarter to report all TDS from business payments made. ” via=”no”]

Here are the due dates for filing Form 26Q.

All the aforementioned due dates are subject to change through the government’s official notification.

All the aforementioned due dates are subject to change through the government’s official notification.

Also read: TDS – An All Inclusive Primer for Businesses

Sometimes it is challenging to keep up with compliance as well as focus on core business operations. This results in delay or non-deposition of taxes collected or loss of growth opportunities.

So, instead of waiting for things to slip from your hands, you should switch to automated software that will make your business fully compliant.

Now that we have given you a piece of advice, we have a perfect fit for it too.

RazorpayX Payroll is an automated payroll & compliance software that lets businesses manage their payroll process seamlessly. Not only payroll, but it also takes care of contract payment disbursements.

The software uses a Direct Deposit model that processes payroll and compliance payments within due dates, as long as the user maintains the wallet balance.

With RazorpayX Payroll, you will never miss out tax deductions, TDS payments to the government and quarterly return filings.

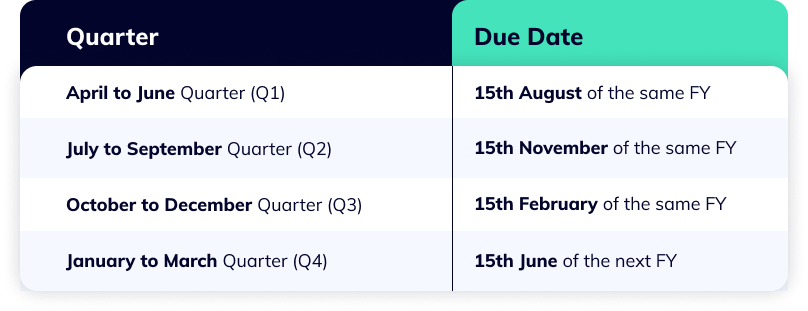

TDS Certificate- Form 16A

Form 16A is a TDS certificate issued by the deductors, which could be a bank, company, or an individual who has deducted tax at source from payments made and deposited to the government.

This form contains TDS amount deducted, nature of payment, and TDS actually deposited to the government.

In the context of this article, businesses are the deductors, and contractors/professionals/owners are the deductees. Form 16A reflects total earnings and total income deducted from business payments in a particular quarter. This information helps deductees to prepare and file their income tax returns accurately.

The due dates to issue TDS certificate – Form 16A.

RazorpayX Payroll simplifies compliance for businesses. You don’t have to worry about PF, ESI, TDS and PT ever again. Along with all the features mentioned above, it also deals with Form 16A generation that can be easily shared with your contractors, subcontractors, professionals and owners.

RazorpayX Payroll simplifies compliance for businesses. You don’t have to worry about PF, ESI, TDS and PT ever again. Along with all the features mentioned above, it also deals with Form 16A generation that can be easily shared with your contractors, subcontractors, professionals and owners.