The Goods and Services Tax, or GST, is a comprehensive tax levied on goods and services in India. It has three components: the Central Goods and Services Tax (CGST), the State Goods and Services Tax (SGST), and the Integrated Goods and Services Tax (IGST).

Once you’ve made the required GST payments, you’ll find out if you’re eligible for a GST refund. If you qualify for a refund, you must file GST refund form RFD-01 on the GST portal to submit an online application for GST reimbursement.

You can claim GST refunds for several reasons, such as errors in tax payments, surplus cash balances, unused Input Tax Credits (ITCs), etc. Additionally, it is essential to choose the right form to submit based on the specific type of refund you’re claiming.

You must file for the GST refund accurately and timely. Delays or inaccurate data might lead to refund denial, resulting in financial losses and compliance difficulties.

Table of Contents

What is the GST Refund Process?

A GST refund is a claim to reclaim excess taxes paid by a taxpayer for various reasons, such as exports, excess input tax credits, or other specific circumstances. Businesses must file claims for GST refunds to protect their finances and guarantee that they are adhering to tax laws.

The objective of the GST system’s refund provisions is to harmonise and standardise the processes involved in filing returns. Businesses or individuals must file a refund claim using the appropriate forms, such as Form GST RFD-01, along with supporting documentation in order to be eligible for a GST refund.

GST Refund Time Limit

The claim for a GST refund must be submitted within two years following the relevant date. This is in accordance with the CGST Act of 2017 Section 54. The relevant date may vary based on the kind of refund that is requested. For the majority of refunds, the relevant date is the day the tax is paid or the date the goods or services are received.

Additionally, you can claim unused ITC at the end of any tax period as per Section 54(3) of the CGST Act, 2017. Subject to a few limitations, if the credit accumulation results from zero-rated supply or an inverted duty structure, the unused ITC may be claimed.

Related Read: Inverted Duty Structure Under GST Explained

What situations lead to refund claims?

A claim for a refund may arise due to a variety of reasons, which include:

-

GST merchant export of goods or services.

-

Supplies to SEZs units and developers.

-

Deemed exports.

-

Excess tax paid in advance by a casual taxpayer.

-

If CGST & SGST were paid, treating supply as intrastate or interstate incorrectly.

-

Issuance of refund vouchers for taxes paid on advances not utilised for supply.

-

Judgement, decree, or order of appellate authority or court.

-

Finalisation of provisional assessment.

-

Accumulated ITC due to inverted duty structure.

-

Pre-deposits.

-

Refunds to International tourists for GST on goods taken abroad.

-

Refund of taxes on purchases by the UN or embassies.

What are Steps to Submit a Refund Pre-Application Form

Taxpayers must fill out the Refund Pre-Application Form in order to provide particular details about their business, such as Aadhaar number, income tax information, export data, expenses, and investments. The original GST refund invoice must be filed before this form is submitted.

Before filing for the original application to get a GST refund, you are mandatorily required to submit the pre-application form. Furthermore take note that once submitted, this form cannot be modified and doesn’t have to be signed. Thus, be careful when entering the information.

The pre-application form must be submitted before the real application for a GST refund. Please note that once this form is submitted, it cannot be modified and does not need to be signed. Therefore, the user must exercise caution when inputting the details.

Filling out the pre-application form for a GST refund consists of the following steps:

Step 1: Go to the GST portal, navigate to ‘Services’ > ‘Refunds’ and choose ‘Refund pre-application form’.

Step 2: Fill in the required details on the ‘Refund pre-application form’ page. Click ‘Submit’ and confirm your submission on the screen.

Particular details that should be reported on the form include the following:

-

Specify the nature of your business, such as manufacturer, trader, merchant exporter, or service provider.

-

Date of issue of IEC (only for exporters) required if you are claiming export refunds.

-

Aadhaar number of the primary authorised signatory is mandatory.

-

Value of exports in FY 2019-2020 (only for exporters), computed at the GSTIN level.

-

Income tax paid in FY 2018-2019.

-

Advance tax paid in FY 2019-2020.

-

Investments and capital expenditure made in FY 2018-2019.

Refund Process of IGST on Export of Goods (with tax payment)

Exports are deemed ‘zero-rated supply’ under GST. Therefore, exporters can claim a refund of the Integrated Items and Services Tax (IGST) and cess paid on the exported items. This repayment mechanism is intended to guarantee that the Indian tax system does not serve as a barrier to exports.

Since exporters have a large number of transactions, the GST portal makes the GST refund procedure easier. In this case, there is no need for a separate RFD-01 application. However, in order to receive a GST refund, the exporter must meet particular requirements.

-

Table 6A in GSTR-1 must be filled with shipping bill details for export transactions (tax paid) due by the filing deadline.

-

Report summary details in item 3.1(b) of GSTR-3B.

-

Pay the corresponding tax by GST law’s due date.

-

In export invoice data under Table 6A of GSTR-1, provide the complete shipping bill number, date, and port code.

-

File export transactions in the GSTR-1 and GSTR-3B of the same tax period.

-

Ensure total IGST and cess in GSTR-3B (Table 3.1) match or exceed GSTR-1’s Table 6A and Table 6B.

-

The shipping bill serves as a refund application per GST authority.

-

GST portal sends export details to ICEGATE from GSTR-1.

-

Confirmation of GSTR-3B filing for the relevant tax period is sent.

-

The Customs system matches GSTR-1 with the shipping bill and Export General Manifest (EGM) for refund processing.

-

ICEGATE informs the GST portal of refund payment details.

-

GST portal notifies taxpayers via SMS and email upon refund crediting.

Steps to Apply in Form RFD-01 for Various GST Refund Claims

RFD-01 is the form used for filing different kinds of GST refund requests. It is essential that you apply for a refund accurately, depending on the nature of the claim, in order to ensure proper processing and prompt refunds.

The RFD-01 must be filed for the following categories of refunds under GST claims:

-

If your electronic cash ledger has an excess balance due to excess cash payments.

-

If you paid IGST on the export of services along with the payment of tax.

-

If you have accumulated ITC due to excess tax paid on inputs than outward supplies.

-

Accumulated ITC from supplies to SEZ units/developers without tax payment.

-

ITC accumulation due to inverted tax structure (higher tax on inputs than outputs).

-

Receiving deemed exports.

-

Tax paid on supplies to SEZ units/developers with tax payment.

-

Tax paid on an intrastate supply is later reclassified as interstate, and vice versa.

-

Suppliers of deemed exports are eligible for a refund if the tax is paid without collecting from the buyer (with a declaration from the buyer).

-

Refund due to Assessment, Provisional Assessment, Appeal, or other orders.

-

Refund on ‘Any other ground’ using RFD-01.

-

Refund claim by unregistered taxpayers.

There are certain certification and documentation requirements for every type of refund claim. For example, in some situations, certification from a cost accountant or chartered accountant may be necessary. To guarantee efficient processing, complete information on the invoices in GSTR-1 and RFD-01 must be provided.

To submit a refund application in RFD-01, follow these steps:

-

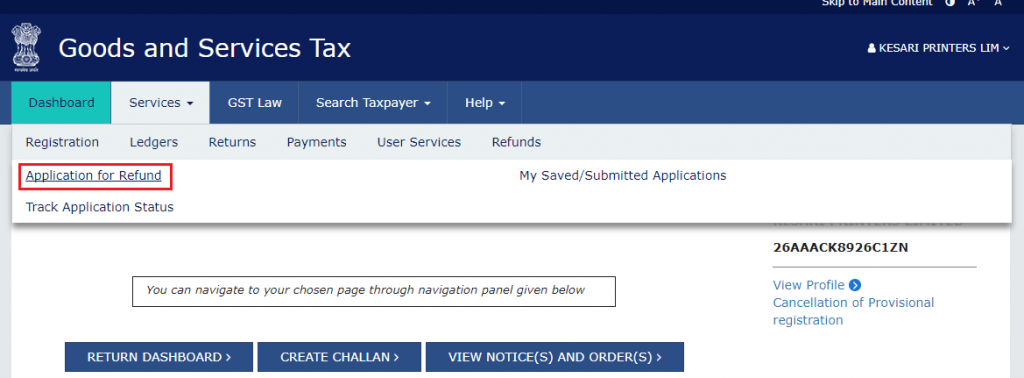

Step 1: Log in to the GST portal, go to ‘Services’ > ‘Refunds’ > ‘Application of refund.’

-

Step 2: Select the reason or type of refund and click ‘Create refund application.’

-

Step 3: Choose the refund period and indicate if it’s a nil refund. For nil refunds, checkmark the declaration and file using DSC or EVC.

Note: This step is not applicable for certain refund types like excess cash balance, change in supply type, assessments, appeals, or other orders.

-

Step 4: Enter details on the displayed page based on the selected refund type from Step 2.

Types of GST Refund Claims and Application Process – Step-by-Step Guide

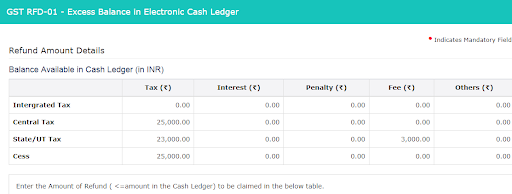

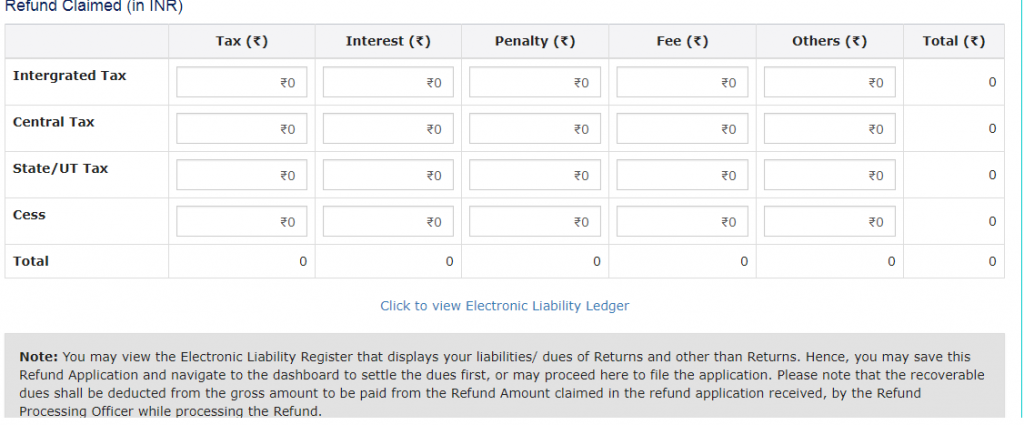

Type 1: Excess Cash Balance in Electronic Cash Ledger

Enter the amount of cash to be claimed as a refund.

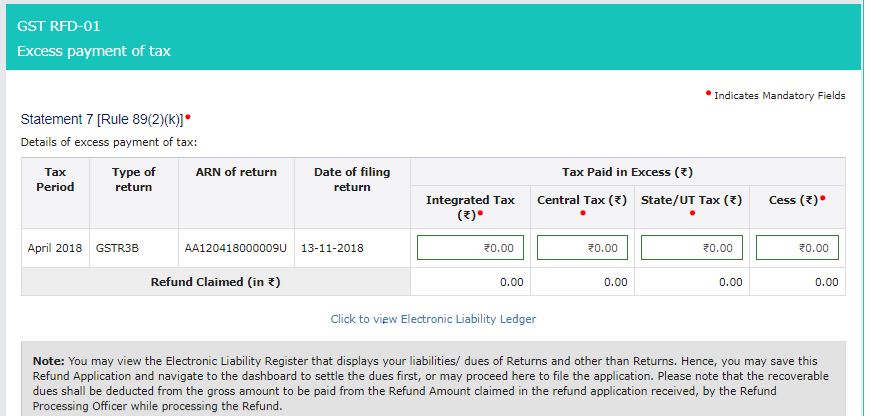

Type 2: Excess Tax Paid Through GSTR-3B

Enter details of the GSTR-3B with excess tax payment in cash.

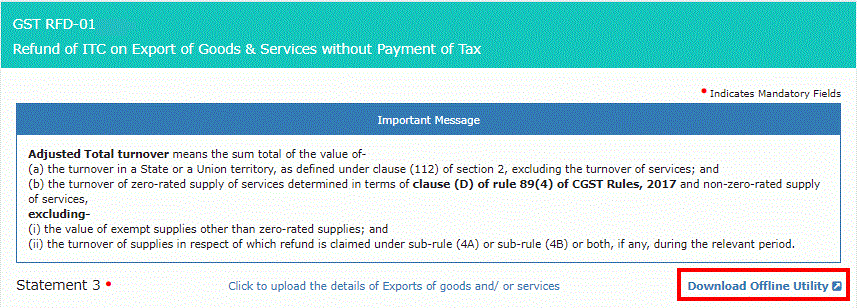

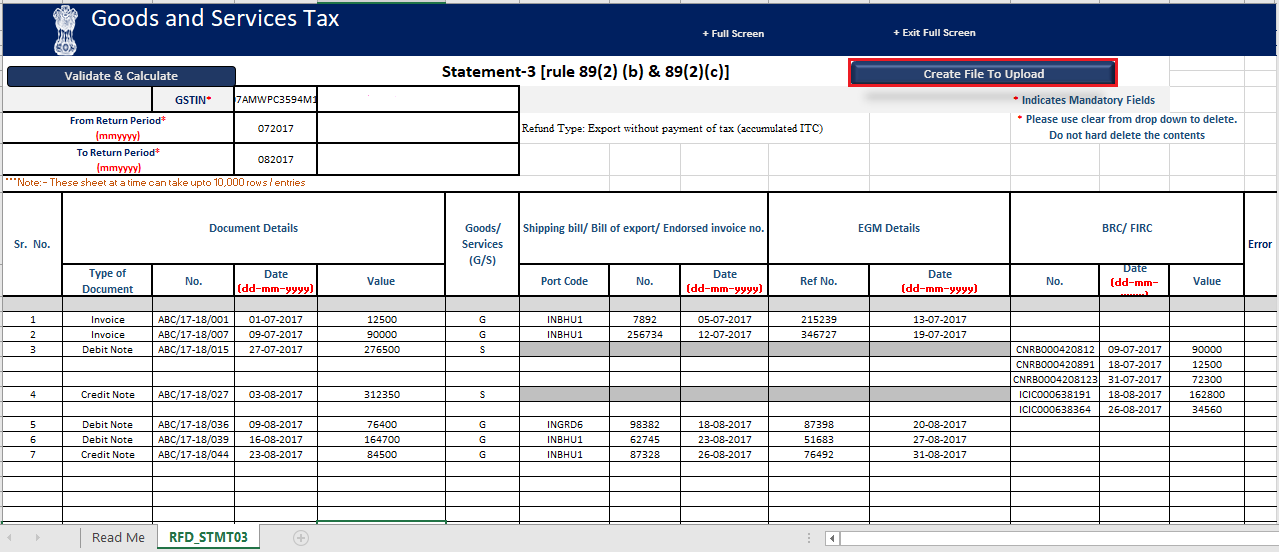

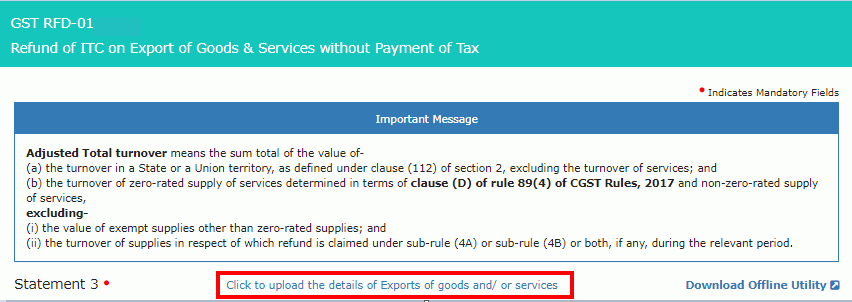

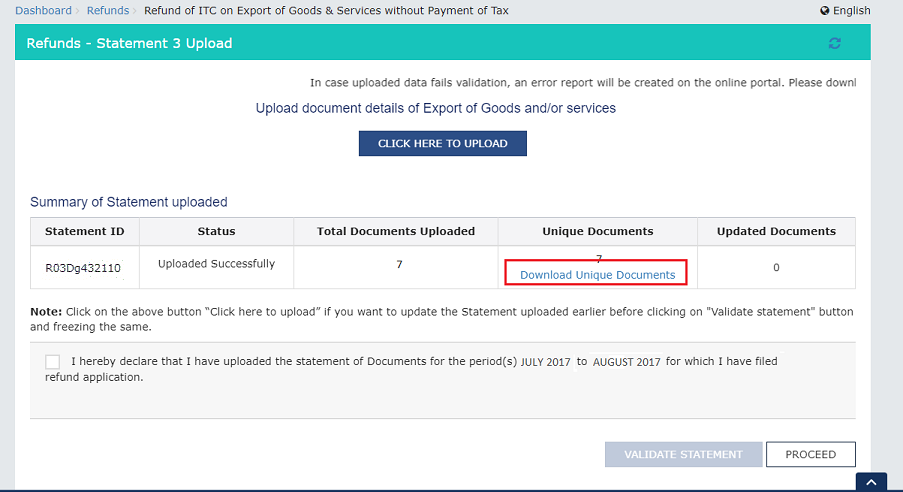

Type 3: Accumulated ITC Due to Exports

Step A: Enter export invoice details in Statement 3.

Step B: Generate and upload a JSON file on the GST portal. Validate errors, if any.

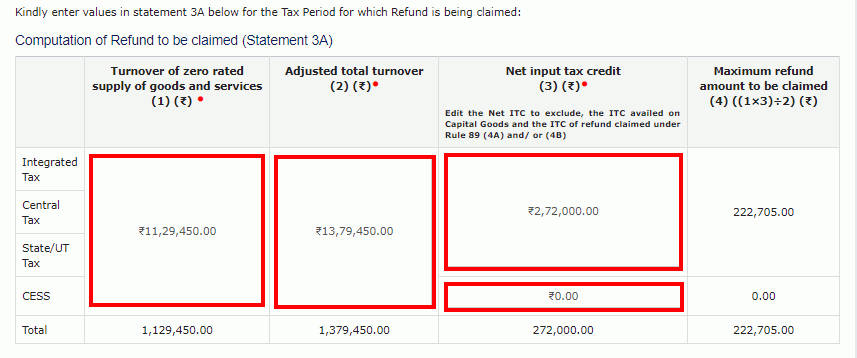

Step C: Fill out the ‘Computation of Refund’ in Statement-3A with turnover and input tax credit details.

Step D: Validations determine the eligible refund amount.

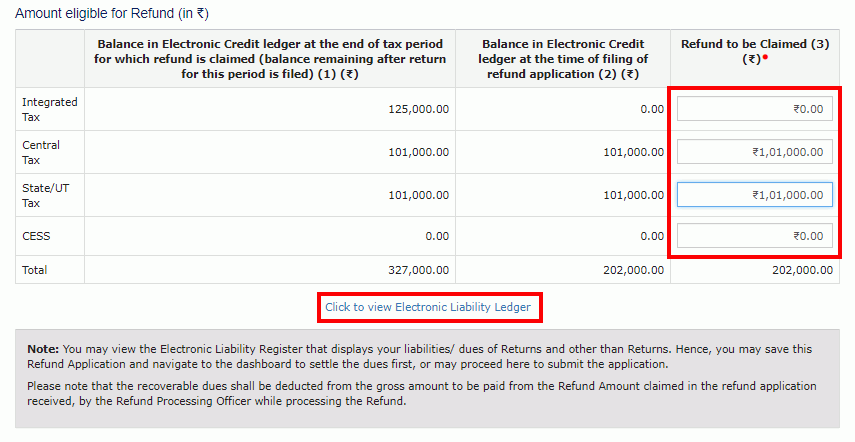

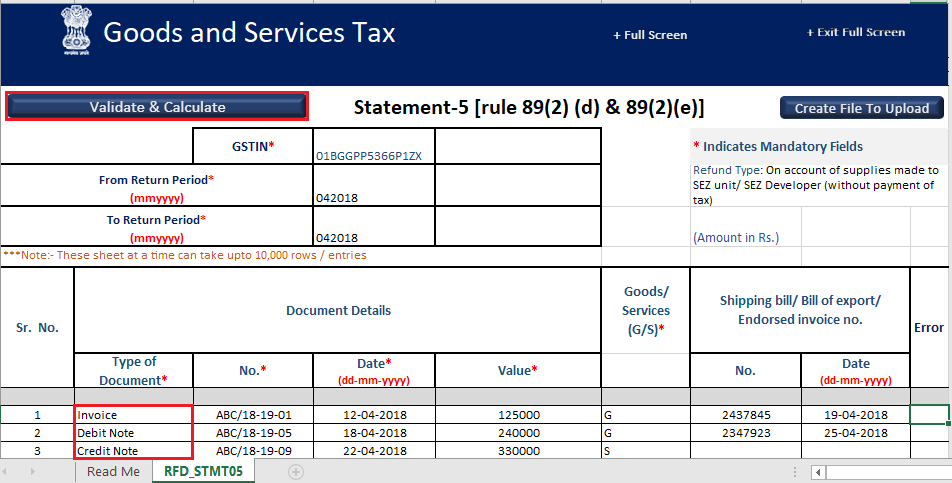

Type 4: Accumulated ITC Due to Supplies to SEZ

Make sure you file GSTR-1 and GSTR-3B for the selected period. Follow the same steps as for the Type 3 refund; however, utilise Statement 5 and accept CSV files rather than JSON.

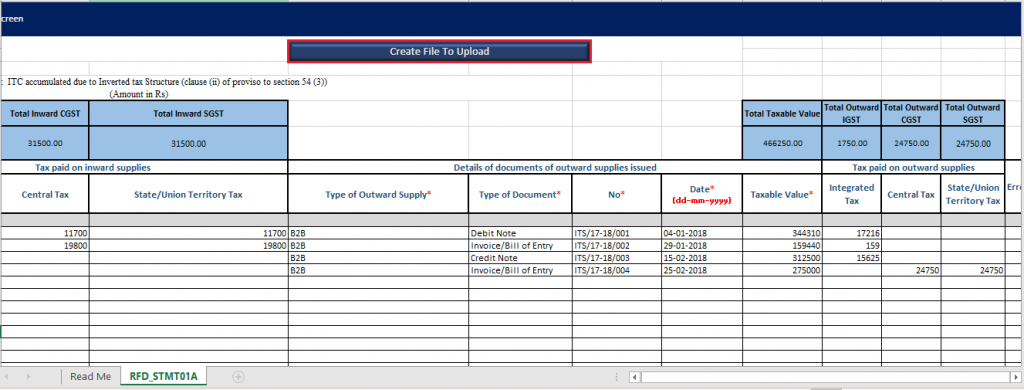

Type 5: ITC Accumulated Due to Inverted Tax Structure

The inverted tax structure means greater tax rates and payments on inputs than on output. The process is similar to that of a Type 3 refund, including Statement 1A and data such as turnover of inverted rated supply, tax due, adjusted total turnover, and net ITC.

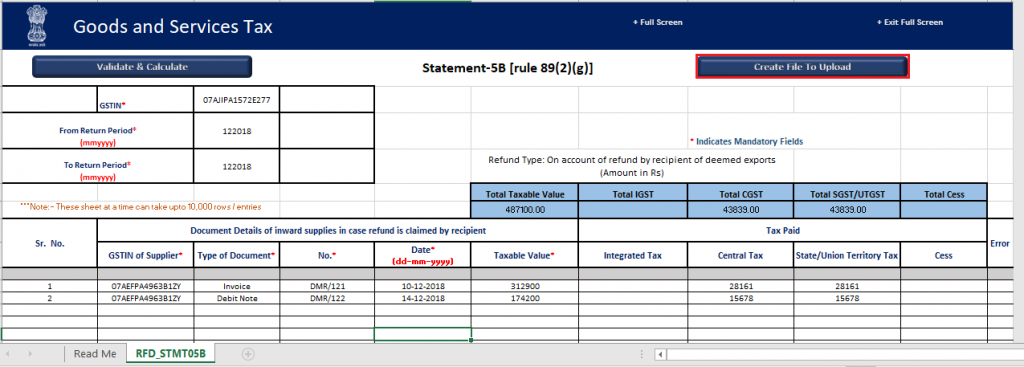

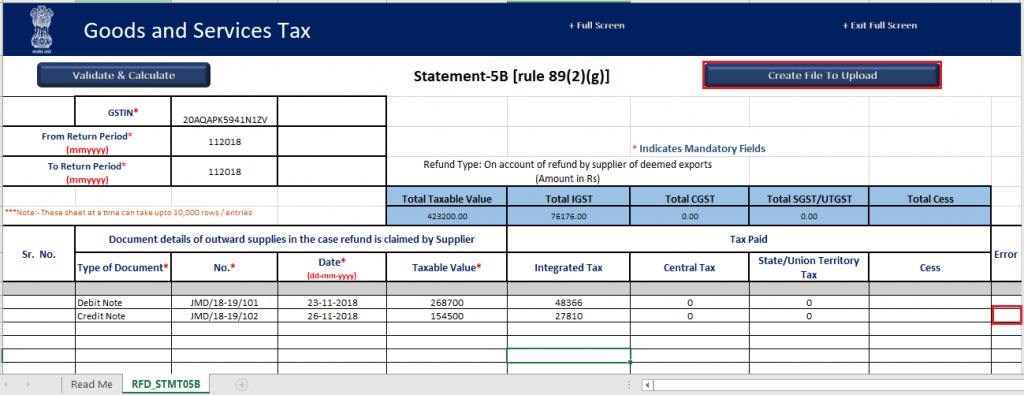

Type 6: Refund by the Recipient of Deemed Exports

If the recipient of deemed exports pays tax on inbound supplies that qualify as deemed exports and claims ITC in their electronic credit ledger, they are entitled to a refund of the tax paid. However, the supplier of considered exports cannot obtain a refund.

Use Statement 5B and follow the same steps as for the Type 3 refund (mentioned above). Add information such as the amount of the requested refund and the net input tax credit for presumed exports.

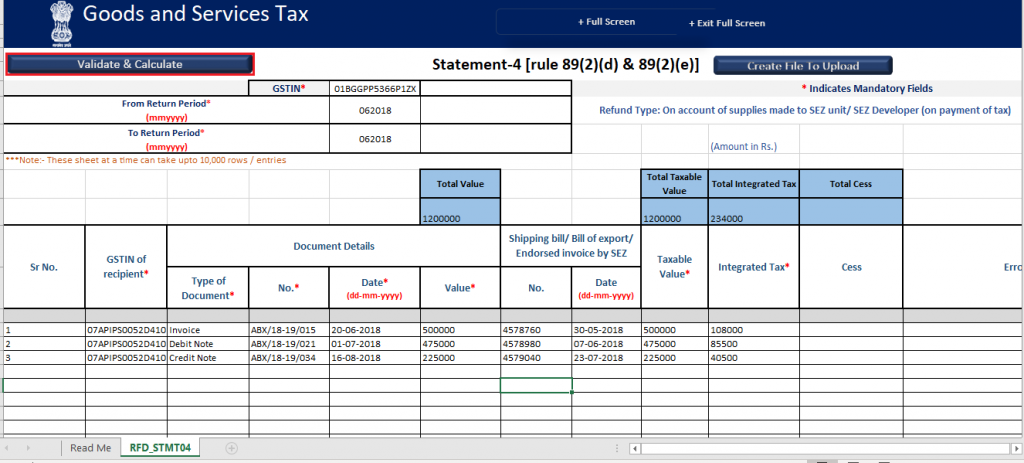

Type 7: Tax paid on supplies made to SEZ unit/SEZ developer (with payment of tax)

The steps to follow are still the same as those outlined above for the Type 3 refund. However, Statement 4 will be the statement here. The submitted statement will be used to automatically generate the refund amount.

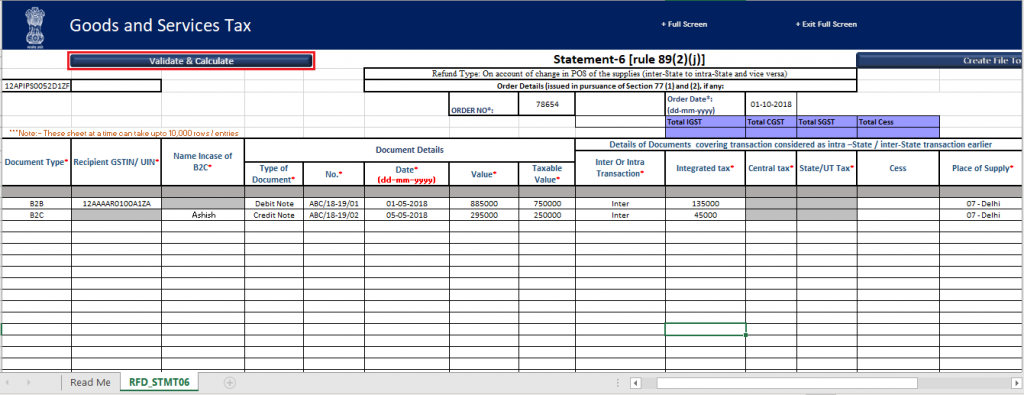

Type 8: Tax paid on an intrastate supply later held as interstate supply and vice versa

The method is similar to that of Type 3 refunds, as previously explained. Use Statement 6, and the refund amount will be auto-filled from the uploaded statement.

Type 9: Refund by the supplier of deemed exports

The process is similar to that of a Type 3 refund mentioned above, with Statement 5B used and the refund amount auto-filled from the submitted statement.

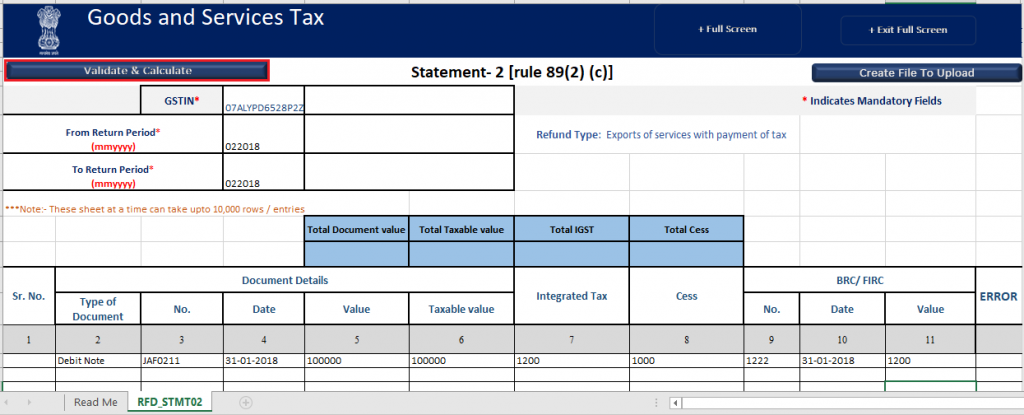

Type 10: Refund of IGST paid on export of services (with tax payment)

The procedure is similar to that for Type 3 refunds. Statement 2 will be utilised, with the refund amount auto-filled from the supplied statement.

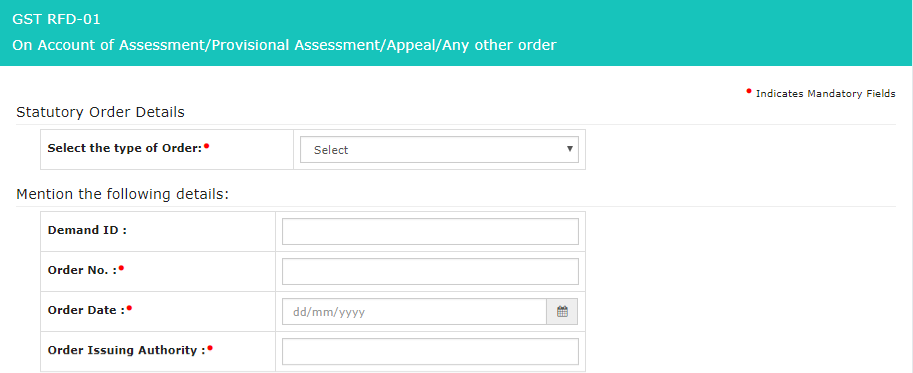

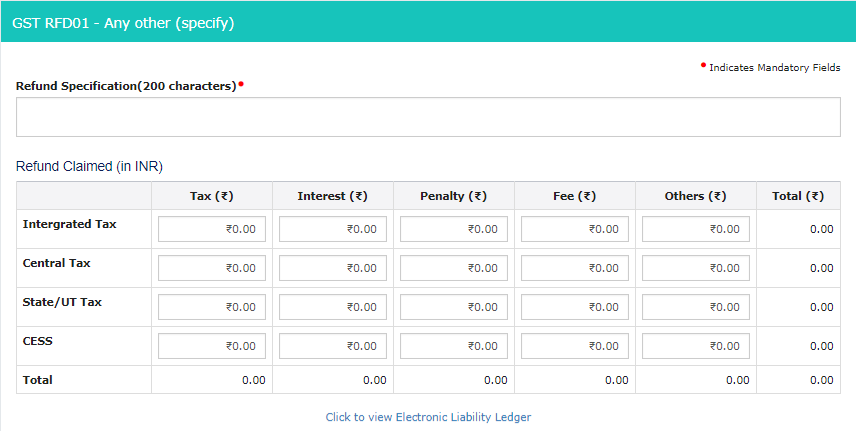

Type 11: On account of assessment or provisional assessment or appeal or any other order

Select the type of order and input the details, as shown in the image below:

Type 12: Refund on ‘any other ground’

The GSTR-3B may have been used to pay excess interest. Give a precise 200-character explanation of the refund’s purpose and include the amount.

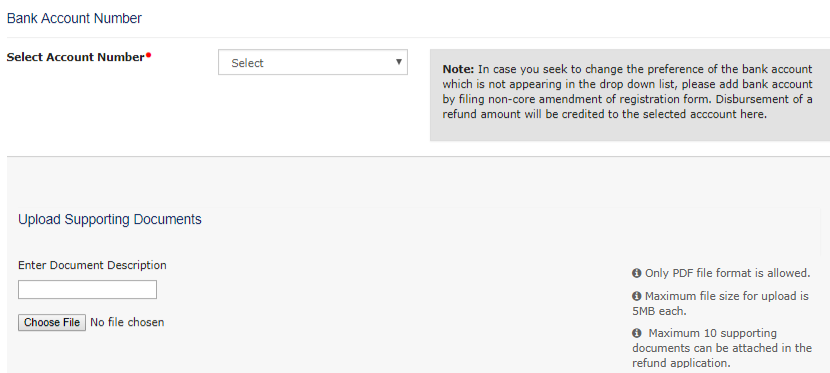

Additional steps to submit a refund application in RFD-01 include:

-

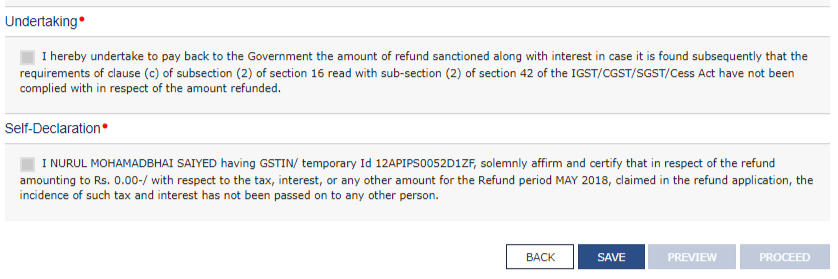

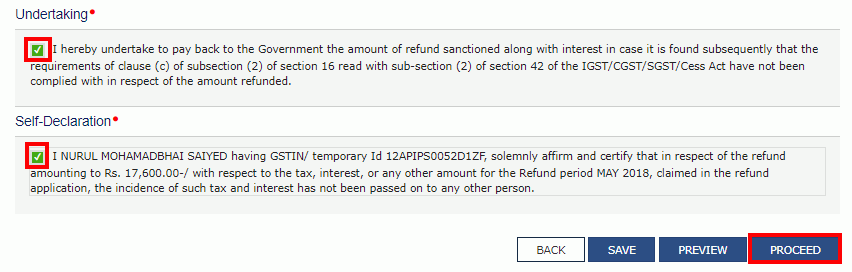

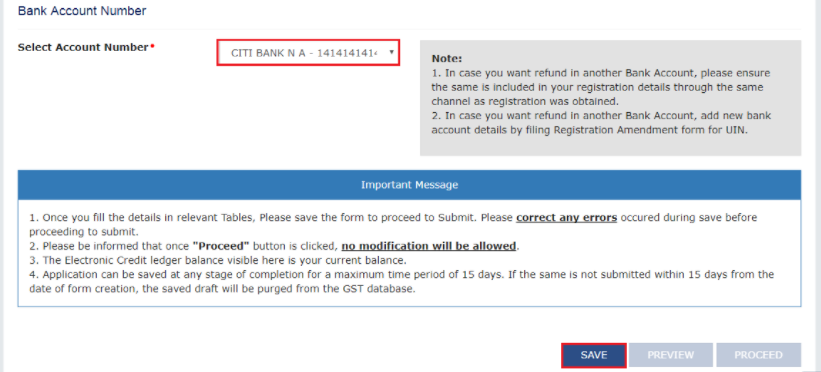

Enter bank details for refund, upload required documents and declaration where necessary. You can upload up to 10 supporting documents, each up to 5 MB in size. Preview and save your application. It will be available for 15 days. Now click ‘Proceed’ after confirming the undertaking and self-declaration checkboxes.

-

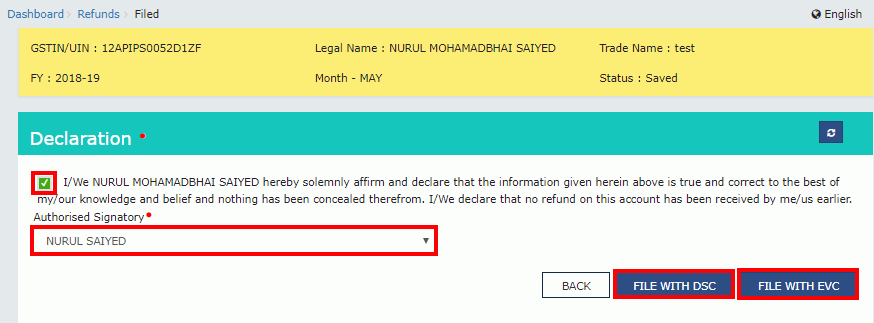

File RFD-01 using EVC or DSC.

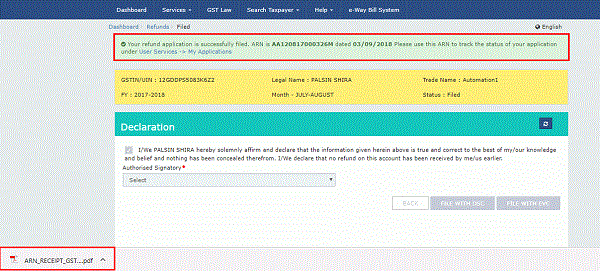

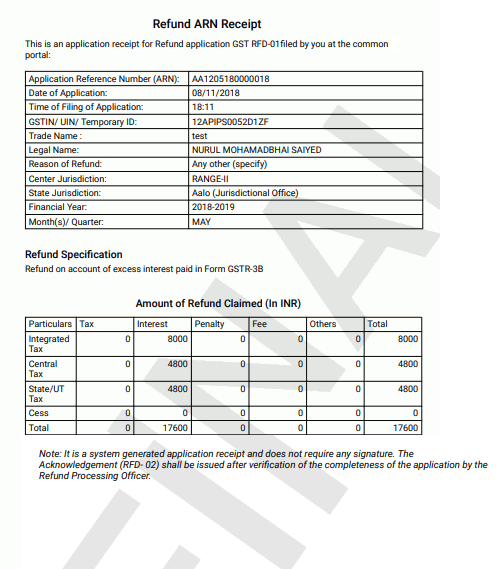

The ARN appears on the screen and can be used to track the application. It’s also sent to the email and mobile.

The refund application is assigned to the processing officer, who updates its status after processing.

Refund Claim by Unregistered Person

The refund process in GST for embassies and foreign organisations is unique and necessitates specialised steps and forms. These entities are entitled to refunds under GST on taxes paid on inward supply of goods and services obtained for official purposes.

There are two ways to claim refunds in this case:

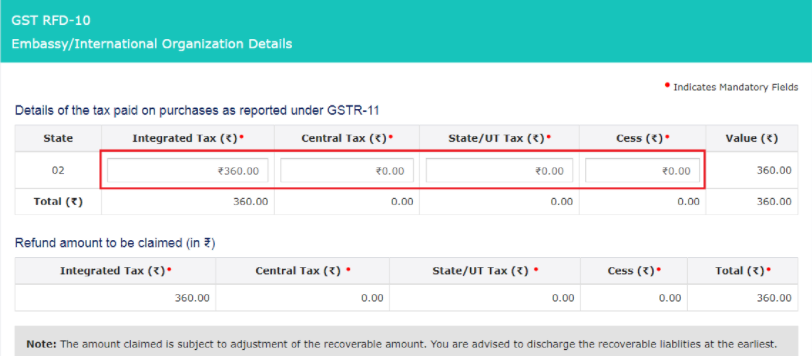

Method 1:

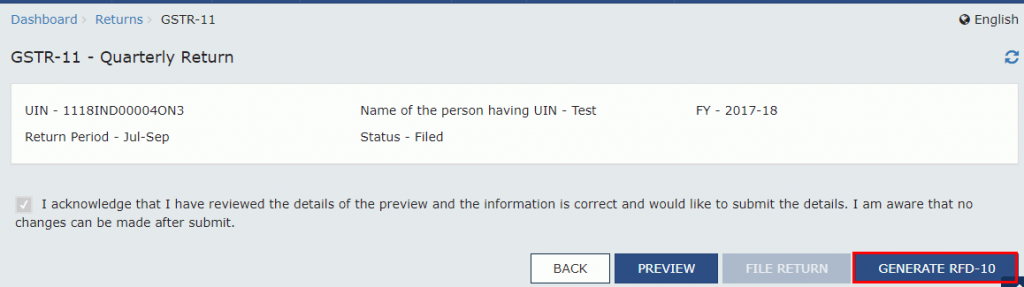

Use GSTR-11 and select the tax period/quarter. Click ‘Generate RFD-10’.

Following the first step, go to the filed GSTR-11, select the tax period/quarter, and click ‘Generate RFD-10’.

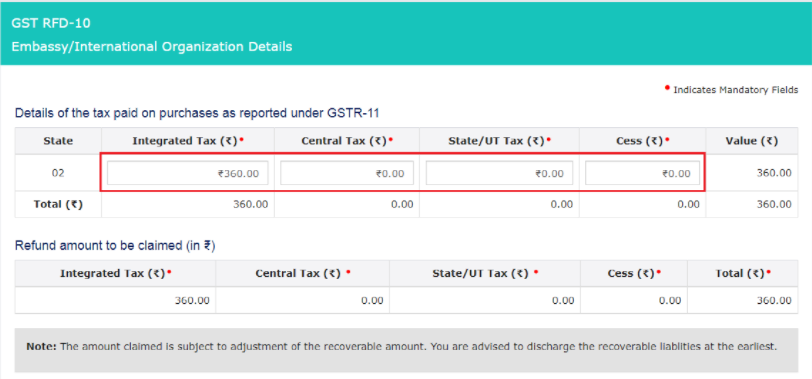

Choose the embassy or organisation radio button and click ‘Create’. The table ‘Details of tax paid on purchases under GSTR-11’ will auto-populate amounts from the respective return period, which you can edit as needed.

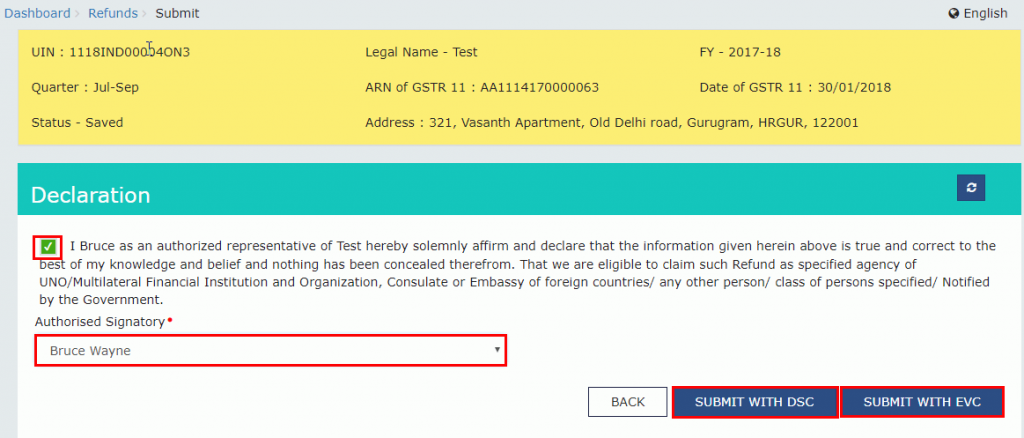

Now, preview and submit using DSC or EVC.

Method 2:

Access the RFD-10 form on the dashboard after logging into the GST portal.

After logging in to the GST portal, navigate to the ‘Services’ tab, select ‘Refunds’, and then choose ‘Application for refund’.

Select ‘Embassy/International Organisation’ and click ‘Create’ on the displayed page.

Tax refund details will get auto-filled from filed GSTR-11. You can verify, edit, or enter a refund amount as needed.

The rest of the steps remain the same as the first method.

Post-GST Refund Application Process

The application submitted by you will show up as a pending work item on the tax officer’s or refund processing officer’s dashboard. He or she will check and examine the documents and the application. By using the “Track Application Status” option under Refunds, you may keep tabs on the progress of their application.

The officer’s actions will be as follows:

-

Provisional Refund (RFD-04): Granted within 7 days, 90% of the claimed amount.

-

Acknowledgement (RFD-02): Issued within 15 days if the application is complete.

-

Withdrawal Option (RFD-01W): Applicant can withdraw refund application (credited to the ledger).

-

Deficiency Memo (RFD-03): Issued within the same time limit, auto re-credit if debited (fresh application needed).

-

Clarification Notice (RFD-08): Issued for rejection/recovery; applicant must reply within 15 days (RFD-09).

-

Sanction/Rejection Order (RFD-06): Followed by Payment Order (RFD-05) in sanction cases; RFD-05 sometimes issued after RFD-04.

-

Withholding Order (RFD-07 Part-B): May withhold sanctioned refund; no RFD-05 issued.

-

Re-Credit Order (PMT-03): Re-credits refunds in rejection/provisional refund cases.

Frequently Asked Questions (FAQs):

1. How can I claim a refund of the excess amount available in the Electronic Cash ledger?

Go to the “Refunds” area of the GST portal, log in, and choose the “Refund of Excess Balance in Electronic Cash Ledger” option to obtain a refund of the excess balance in the Electronic Cash Ledger. Once the GST RFD-01A form is completed, you must submit the application and include the information about the excess amount that has to be repaid. Once you have registered your bank account with the GST site, the refund amount will be refunded back to it.

2. What is the amount limit to claim the refund?

The maximum refund for an excess GST payment is ₹1000. Refunds cannot be claimed for amounts below this. For excess payments over ₹2 Lacs, a Chartered Accountant (CA) must verify the amount, and a CA certificate must be included with the refund form.

3. What are the required documents to upload during the GST Refund Application?

-

Printout of GSTRFD-01 A & ARN.

-

GSTR-3B/GSTR-3 printout for the specified month.

-

Statement-2 as per Rule 89 (2) (c).

-

Undertaking as per para 2.0 of circular 24/2017.

-

Export & input service invoices.

-

BRC/FIRC: Proof of payment received from export.

-

Undertaking of no prosecution as per Rule 91(1)[5].

4. How to know the available balance in my Electronic Cash Ledger?

-

Login to the GST Portal and enter your credentials.

-

Go to “Services” and select “Ledgers.”

-

Click “Electronic Cash Ledger” and check the “Cash Balance as on Date” column.

5. How to track the GST refund application status?

To track your GST refund status:

-

Log in to the GST Portal.

-

Go to “Services” > “Refunds” > “Track Application Status.”

-

Enter ARN or select the financial year of the refund application.

6. How to download my filed refund application?

-

Log in to the GST Portal.

-

Navigate to Services > Refunds > My Applications.

-

View filed refund applications.

-

Click “Documents” under “Download” to get the PDF of your refund application and supporting documents.

7. Am I able to enter bank account details while claiming the GST refund?

Yes, you can enter your bank account details while claiming the GST refund. To do so, you need to:

-

Navigate to the GST Portal and select “Refunds.”

-

Click on “Track Application Status.”

-

Enter the ARN or fiscal year.

-

Click “Update Bank Account” under “Bank Validation Status.”