Planning on starting an online business? Confused if you should open a Nodal, Escrow, or Current account? We’ll help you understand what each of these terms means and which accounts suit your business type.

Before that, let’s take a step back and understand how it all started.

If you were running a business two decades back, everything – from receiving payments from customers to making vendor payments would mostly be done through cash or bank cheques. Opening and managing a bank account was tedious and time-consuming.

Then came the internet era.

The physical barrier of reaching only a small set of customers through a physical store is completely offset in the online world.

Everything from hailing a cab to buying groceries to even attending an educational course can be purchased and paid for online. This convenience, however, requires sound and efficient operations in the backend.

Several entities from sellers to vendors to logistics partners and payment processors have to work together. And, money has to be moved across from the customers to all these parties in order to ensure success of a business.

Nodal and Escrow are special kinds of bank accounts that have been specifically built to handle the complex money transfers that online commerce players face.

So, let’s understand how these accounts work.

Nodal Account

By definition, nodal accounts or nodal bank accounts are special internal bank accounts that are mandated by the RBI for businesses that are intermediaries, connecting customers to sellers.

So, what really is an intermediary? Well, your online business would be an intermediary if:

- You collect money online from customers on behalf of your vendors.

- Where you are only sourcing the products and not actually manufacturing them.

- Where you do not fully pay for the products or stock inventory of the products.

The striking feature of online commerce is the multi-layered interactions between several unknown parties – customers, vendors, payment gateway etc. If payouts between these parties aren’t down on time, it will lead to an erosion of trust.

The purpose of a nodal account is to cover for the ‘trust’ factor. It safeguards the interests of customers and vendors so that payments are collected, processed and payouts are done to relevant vendors without undue delay.

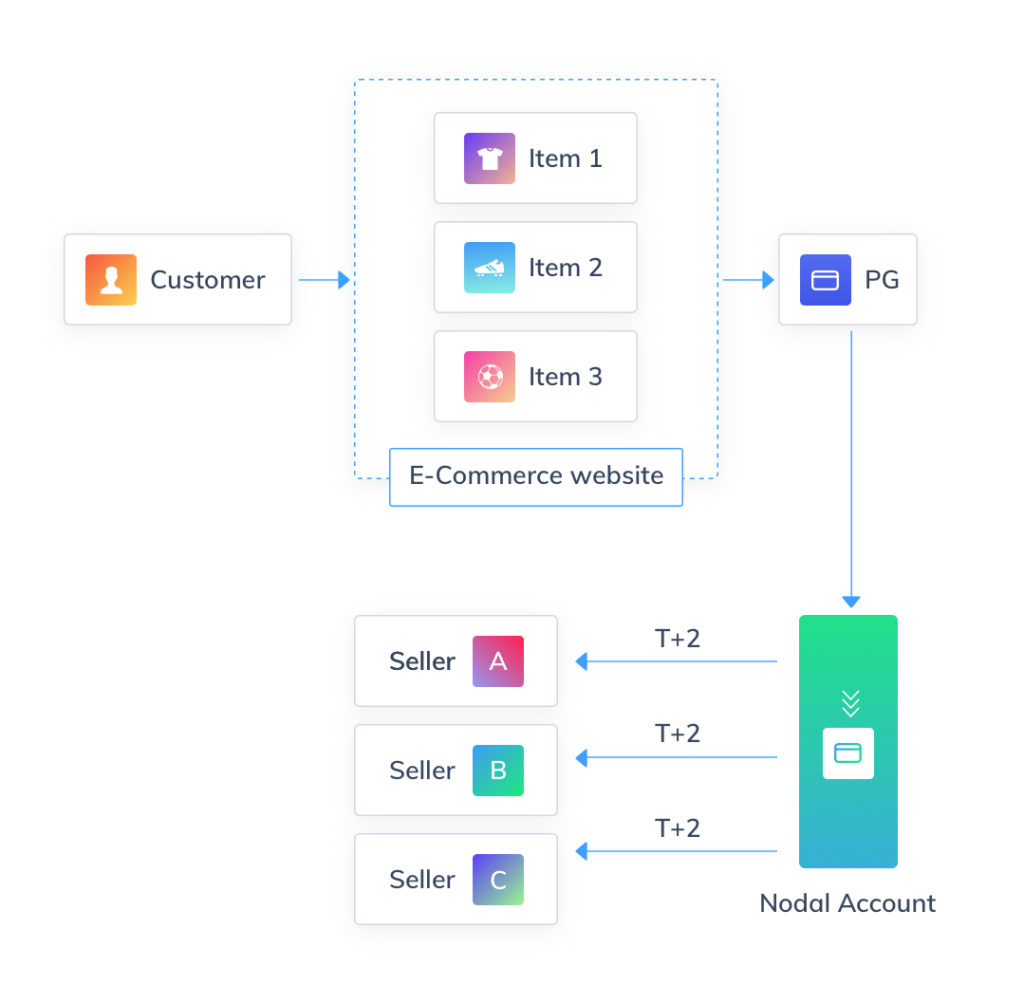

The transaction flow of a nodal account at a marketplace is illustrated below:

Essentially, the nodal account acts as a temporary vault to store and distribute the money to relevant parties.

Payouts are not only limited to sellers/vendors. But, they also include other entities like transportation fees to logistics partners, commissions to payment processors and charges to intermediaries etc.

There are some important terms to understand in relation to nodal accounts. We’ve explained them below:

Intermediary – An intermediary is an entity that collects money from customers online and then transfers it to the sellers and vendors involved. Online aggregators and marketplaces are good examples of intermediaries. Exceptions to this are businesses that facilitate the delivery of products or services immediately, like the sale of movie tickets.

Settlement Cycle – As defined by the RBI, the settlement cycle for payments channelled through nodal accounts is T+3 days. T is defined as the completion of the transaction, where the customer has received the product or service as defined by the intermediary.

Debits – Debits can be made to bank accounts of vendors, sellers, other partners based on agreed terms and conditions. This also includes refunds for disputed transactions. The business can only raise a request for debit, the final approval for debit has to come from the bank.

Credits – Credits can be made into the nodal account based on pre-determined terms and conditions.

Opening a Nodal Account

A business can request a nodal account from any bank approved by the RBI. Different banks impose different criteria to approve nodal account requests.

Qualification criteria might range anywhere from the amount of capital investment to business reputation to transaction volumes to be processed. Businesses will also be required to submit all KYC documents and agree to strict compliance requirements through concurrent audits as mandated by the Payments and Settlements Systems Act, 2007.

Opening and maintaining a nodal account requires significant effort from businesses. Integration with the bank’s systems could be tedious and host to host server integration not always feasible (hence transaction details have to be manually uploaded for the bank to then approve)

Escrow Account

Have you heard that phrase ‘Escrow’ long before the internet age?

In fact, it is believed that escrow was used as early as the Middle Ages. ‘Escroe’ meant a small piece of paper, scrap or parchment that acted as a deposit of trust or security and was held by third parties until a future condition was satisfied.

Even today, in online commerce, the underlying philosophy of an escrow account is to ensure trust and security. An escrow account is a temporary vault of money held by a trusted third party on behalf of two transacting parties that are bound by a contract. Generally, an escrow account is used for the following circumstances:

- When the buyer and seller haven’t met before

- When the contract is complex and long-term

- When the contract has a high value and payment

- Where payment has to be made in accordance with the stage of completion of the project (Eg. a real estate purchase)

A good example where escrow accounts are commonly used is the real estate industry. Let’s take the case of a house, that is being built by a real estate developer.

A buyer who is interested in purchasing the house can use an escrow account to park the money (for the total value of the house) and make payments in parts, based on the level of completion, as outlined in the terms of the purchase contract.

This way, the buyer is assured that there is no loss of money and the seller is assured of the buyer’s ability to pay in full.

Escrow accounts are also used in online commerce. Escrow mitigates the potential risk involved when the buyer is completely unknown to the seller. For instance, if you were buying second-hand furniture from an unknown person, an escrow account is recommended.

The escrow acts as buyer protection and safeguards you from losing money over unsatisfactory, damaged or undelivered products or services. Hence, it also reduces the likelihood of disputes or chargebacks for the seller.

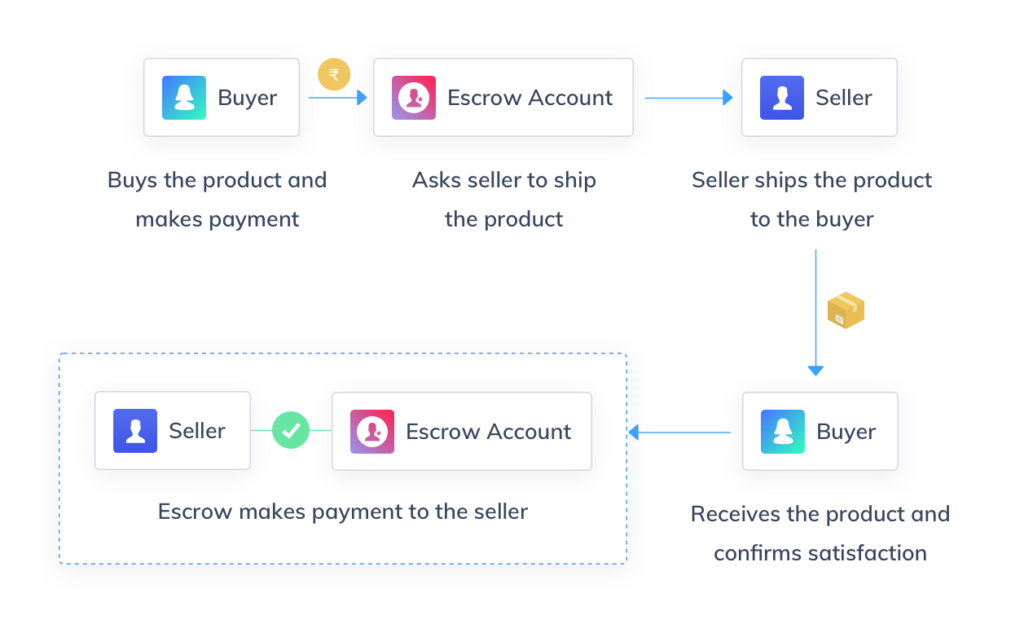

This is how an escrow transaction flow in e-commerce would look like.

Generally, banks and financial service companies serve as escrow agents and provide escrow services for a fee. Make sure to go through the terms and conditions detailed by escrow agents before signing up with an escrow agent.

Current Account

A current account is the most common account used by businesses. Current accounts are liquid accounts with no upper limit on the number of transactions (deposits, withdrawals, transfers, etc.) that can be done in a single day.

Current accounts can be opened at all commercial banks and most banks support multi-location deposit and withdrawal facilities, to suit the varying needs of a business.

Due to the liquid nature of the account, most current accounts do not earn interest. Current accounts support both online and offline/cash transactions – so whether it is depositing a customer’s cheque at a bank or transferring staff salary online, a current account will be able to fulfill the basic needs of running a business.

Current accounts have become the de facto account for businesses to have, regardless of size, nature or type of business. So, every business by default would need a current account. The question really is – does your business need a nodal or escrow account in addition to a current account? So, to recapitulate, your business would require a nodal or escrow account if:

- You are a business intermediary (aggregator, marketplace etc) – bringing buyers and sellers on a single platform.

- The nature of your business involves transactions between two or more unknown parties.

- Your business involves signing contracts that are complicated, long-term or have a high transaction high value.

Opening a business begins with choosing the right business type and ends with choosing the right bank for your business.

Business Banking can shape the financial journey of a business.

Smart payouts, seamless Vendor payments, automated payroll and many more such features have been taking the Fintech space by storm.

RazorpayX is a full-stack banking suite that supercharges the current accounts

- Banking which Provides end-to-end automation with powerful features like Automated Accounting, OTP management, Maker-Checker Flows,

- Corporate Cards with 20X higher limits

- Automated Vendor Payments

- Forex Services

- Payroll – India’s ONLY payroll with Full compliance automation, Employee Insurance management and TDS filing)

With platforms like RazorpayX , you can supercharge your finances.

Are there any specific topics around managing your business finances, payments, and cash flows that you would like to read about? Let us know in the comments below?

Frequently Asked Questions

What is a Nodal Account?

A nodal Account is a type of current account that is used to hold the funds on behalf of customers & vendors (payouts) to safeguard the interests of the two parties.

What is an Escrow Account?

An escrow account is a third-party account where funds are kept before they are transferred to the receiving party.

What is a Current Account?

A current account is maintained by individuals who carry out a significantly higher number of transactions with banks on a regular basis. This type of account is mainly used by businesses.