Table of Contents

What is a Cancelled Cheque?

A cancelled cheque is a cheque that has already been paid by the bank and is marked with the word ‘CANCELLED,’ indicating that it is no longer valid for making payments. This marking is typically written across its face between two parallel lines.

A cancelled cheque leaf is voided by the issuer to prevent it from being misused or cashed, meaning it cannot be used for withdrawals.

Related Read: What is Cheque Bounce?

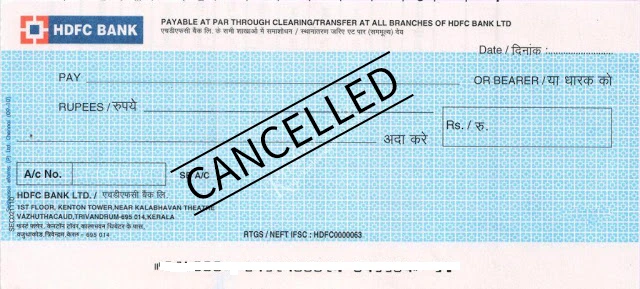

Cancelled Cheque Image and Photo

Here’s a sample image of a cancelled cheque leaf as an example.

Cancelled Cheque Image

What Information Does a Cancelled Cheque Leaf Contain?

The cancelled cheque contains account holder’s information such as account number, IFSC code, bank branch details, cheque number and MICR (Magnetic Ink Character Recognition) code. Notably, it does not require the account holder’s signature.

How to Cancel a Cheque? A Step-by-Step Guide

Here’s a step-by-step guide on how to write and cancel a cheque.

STEP 1: Select a New Cheque

Choose an unused cheque from your chequebook.

STEP 2: Draw Parallel Lines

Draw two parallel lines across the cheque to indicate that it has been cancelled.

STEP 3: Write ‘CANCELLED’

Clearly write “CANCELLED” in capital letters between the parallel lines, ensuring it is legible.

STEP 4: Leave Other Fields Blank

Do not fill in any additional information, such as the payee’s name or amount. The cheque’s purpose is to provide proof of your bank account details only.

STEP 5: Preserve Vital Information

Ensure that important details, including your account number, IFSC code, MICR code, bank name, and bank address, remain visible and unobscured.

What is Cancelled Cheque Used For?

A cancelled cheque is ‘blank’ because it cannot be used as a payment method or instrument. It is often used as proof of payment and to provide bank account details.

However, you will require a cancelled cheque for following use cases.

1. Verification of Bank Account Details

Primary use of cancelled cheques is to verify the individual bank account details. When you open a new bank account, apply for loans, or set up electronic fund transfers (EFTs) you need to submit a cancelled cheque.

Financial institutions like NBFCs also require a cancelled cheque for verifying authenticity of your details.

2. KYC Completion

A cancelled cheque plays a crucial role in completing the requirements of KYC details when investing in stock markets, mutual funds, and other financial schemes.

By submitting a cancelled cheque online, you provide proof of your bank account details to verify your identity and link it to your investment portfolio. This helps financial institutions ensure compliance with regulations and safeguard against fraudulent activities.

3. EPF Withdrawal

Cancelled cheque is mandatory while withdrawing funds from your Employee Provident Fund (EPF) account. It serves as proof of your bank account details, ensuring that the funds are transferred to the correct account.

4. Electronic Clearance Service (ECS)

A cancelled cheque is required to activate the Electronic Clearance Service (ECS) facility for secure fund transfers between bank accounts.

By attaching a cancelled cheque, you authorise the transfer of funds directly from your account to the designated recipient’s account.

5. Automatic Bill Payment

Cancelled cheque can be used to authorise utility bill payments to service providers, subscription-based businesses, and product companies, etc. The company is authorised to debit your bank account for recurring payments such as electricity bills, phone bills, insurance premiums, or membership fees.

6. EMIs

A cancelled cheque is needed to activate Equated Monthly Installments (EMIs) for loans or credit from banks or NBFCs. It facilitates direct debit from your bank account on a specified date, ensuring timely repayment.

7. Demat Account

When opening a Demat account for trading in stocks, a cancelled cheque verifies that you have an active bank account under your name. This ensures seamless transfer of funds during trading transactions.

8. Insurance

Submitting a cancelled cheque is essential when purchasing insurance policies. It acts as proof of your bank account details and aids in premium payments and other transactions related to insurance policies.

Related Read: What are the Legal Documents Required for Starting a Business?

What are the Risks Associated with Cancelled Cheque?

Cancelled cheques cannot be misused. It is important to understand that no transaction can occur with a cancelled cheque. However, it still contains the valid account holder information, and all this information can be misused for fraudulent activities.

Here’s a breakdown of the main concerns:

1. Identity Theft

Be cautious with cancelled cheques, as they contain sensitive details like your account number, bank name, and routing codes. If someone with malicious intent gets hold of this information, they could commit fraud by opening new accounts under your name or stealing your money.

2. Data Breaches

Data breaches are a concern even with trusted organizations. A security lapse on their end could expose the information on your cancelled cheque, even if you provided it to a reputable company.

3. Unauthorized Use

There’s a slight chance that someone you trust with a cancelled cheque could misuse it. While the cheque itself cannot be used for transactions, the account details could be used for unauthorized online payments or money transfers if proper security measures aren’t followed.

Tips For Minimising The Risk Of Fraud Or Misuse When Cancelling A Cheque

When you cancel a cheque, it’s important to take precautions to prevent fraud or misuse. Here are some simple tips to keep your financial information safe:

Always Use Dark Ink

Use a blue or black pen to write “CANCELLED” clearly on your cheque. Dark ink makes it harder for anyone to tamper with the cancellation.

Completely Void the Cheque

Draw diagonal lines or put “CANCELLED” across the entire cheque, covering all spaces where information can be written. This stops anyone from filling in details later.

Protect Sensitive Details

Make sure your account number, name, and other important information remain visible after cancellation. Blocking or hiding these details can cause issues during verification.

Maintain a Record of Cancelled Cheques

Maintain a record of all cancelled cheques along with the date and reason for cancellation. This can be helpful if there’s ever a dispute or question later.

Safely Destroy Unused Cheques

Don’t just toss old cheques. Shred or securely dispose of them to avoid unauthorized use.

Stay Informed About Banking Security

Regularly update yourself on the latest security practices and fraud prevention tips to protect your finances.

What Should I do if a Cancelled Cheque is Lost or Misplaced?

If you’ve lost a cancelled cheque, don’t panic—but do act quickly. While a cancelled cheque usually cannot be used to withdraw money (since it’s marked “CANCELLED”), it still contains sensitive details like your account number, IFSC code, and bank name.

Here’s what you can do:

- Inform your bank immediately and request them to monitor your account for any suspicious activity.

- Let the requesting party know (like your employer or lender) that the cheque is lost and issue a new cancelled cheque if needed.

- Keep a record of the new cancelled cheque you share and, if possible, hand it over in person or through secure means.

Being cautious helps prevent any potential misuse of your account details.

What is the Difference Between a Stop Payment and a Cancelled Cheque

A cancelled cheque is used to share your bank details (like account number and IFSC code) without allowing any transactions. You simply write “CANCELLED” across a blank cheque, and it cannot be used to withdraw money.

A stop payment, on the other hand, is an instruction you give your bank to block a cheque that you’ve already issued. This is useful if a cheque is lost or if you want to halt a payment before it gets processed.

In short:

- Cancelled cheque = Prevents use from the beginning (for verification only)

- Stop payment = Blocks an issued cheque from being processed

Both serve different purposes but are part of secure cheque handling.

Conclusion

A cancelled cheque remains a secure way to share essential bank account details. These details are vital for automated systems, Know Your Customer (KYC) verification, and various banking tasks. By relying on this information, banks can efficiently identify their customers. However, due to the sensitive nature of the information it reveals, it’s crucial to handle a cancelled cheque with caution to prevent potential fraud. When used responsibly, a cancelled cheque becomes a valuable tool for facilitating secure banking experiences.

Frequently Asked Questions (FAQs)

1. Is it mandatory to write a cancelled cheque?

No, it is not mandatory to write a cancelled cheque, but it is often required for various financial transactions.

2. Can my bank cancel my cheque?

Banks can cancel cheques upon customer requests, particularly in situations involving lost or stolen cheques. This provides an added layer of security and helps you protect your financial assets from potential misuse or fraudulent activities.

3. Is it permissible to sign a cancelled cheque?

Yes, it is permissible to sign a cancelled cheque as long as you mark it as “CANCELLED”.

4. What are the risks linked to cancelled cheques?

A cancelled cheque carries the risk of misuse or fraud if not properly destroyed. It may reveal sensitive banking information.

5. Is red ink acceptable for cancelling a cheque?

No, black or blue ink should be used to cancel a cheque.

6. Is it possible to block a cheque leaf online?

No, you cannot block a cheque leaf online. You must physically write “CANCELLED” across the cheque to render it financially invalid.