Business EMI calculator

Business EMI calculator – Plan your loan repayments smartly

Loading Business EMI Calculator…

Check Razorpay products for your business

Razorpay POS

Collect payments swiftly in your store with Razorpay POS and its interesting offers.

Payment Pages

Easiest way to accept domestic & international payments with custom-branded online store.

How to use the business loan EMI calculator

- Enter how much you want to borrow, whether it’s a few lakhs or a few crores.

- Add your lender’s annual rate — usually between 11% and 24%, based on your credit and business profile

- Choose how long you want to repay — typically 12 to 60 months

EMI planning for business growth

- Get accurate monthly payment estimates based on your loan amount, tenure, and interest rate.

- Know exactly how much working capital you can retain while staying consistent with repayments.

- Adjust EMI, interest, or duration to find the best balance for your business goals.

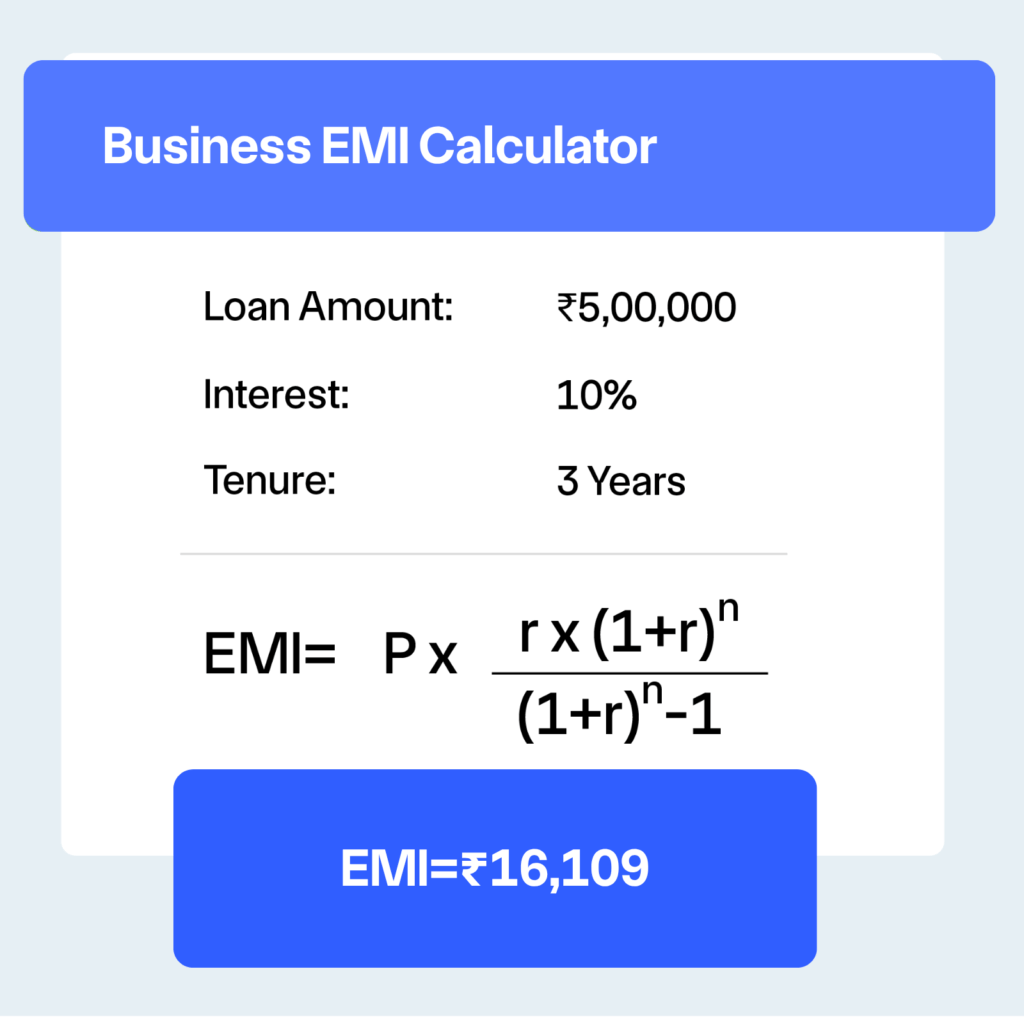

Business EMI formula with example

-

Use the formula:

EMI = [P × R × (1+R)N] ÷ [(1+R)N − 1] -

Where:

P = Principal loan amount

R = Monthly interest rate (Annual rate ÷ 12 ÷ 100)

N = Number of monthly installments -

Example: Business loan of ₹10,00,000 at 15% annual interest for 3 years (36 months).

P = ₹10,00,000 | R = 15% ÷ 12 ÷ 100 = 0.0125 | N = 36 -

Totals:

Total payable ≈ ₹34,665 × 36 = ₹12,47,940

Total interest ≈ ₹12,47,940 − ₹10,00,000 = ₹2,47,940

Tips to reduce EMI interest burden

Improve your credit score

Better score means better loan terms. Pay bills on time and lower credit usage to unlock lower interest rates.

Compare lenders

Check offers from multiple banks and NBFCs. Even a small rate difference can save big over time.

Negotiate better rates

Don’t settle for the first offer. Use other quotes as leverage to get a better deal.

Choose the right tenure

Longer tenures mean smaller EMIs but higher total interest. Find a balance that fits your cash flow.

Make part pre-payments

Use extra business income to prepay a portion of your loan. It cuts down your principal and future interest.

Build a strong banking relationship

Maintain steady transactions and healthy cash flow — banks often reward reliable customers with better terms.

What is a reasonable EMI ?

- Keep your business loan EMI within 25–30% of monthly cash flow to ensure smooth operations and healthy working capital.

- Example: For a business earning ₹2,00,000 monthly, the EMI should ideally stay between ₹50,000–₹60,000 to handle seasonal or unexpected expenses.

- Align EMI payments with your business cycle — use step-up or step-down EMIs if your revenue varies seasonall

Use cases for Business EMI calculation

Machinery purchase

Many small manufacturers take loans to buy new machines or upgrade production units. EMI calculation helps them plan repayments without affecting monthly cash flow.

Office expansion

Retailers and service providers use business loans to open new branches or renovate existing ones. Knowing the EMI in advance ensures steady cash management during expansion.

Managing seasonal demand

Businesses that experience seasonal spikes — like clothing or FMCG — often borrow to stock up inventory. EMI planning helps align loan repayments with sales cycles.

Frequently Asked Questions

Can I change my EMI amount during the loan tenure?

Most lenders offer flexibility through part-prepayment options or tenure modification, subject to terms and conditions.

Are business loan EMI calculators accurate?

Yes, EMI calculators provide accurate estimates based on the input values. However, actual EMIs may vary slightly due to processing fees and other charges

What happens if I miss an EMI payment?

Missing EMIs can result in penalty charges, negative credit score impact, and potential legal action. Always communicate with your lender during financial difficulties.

Can I get tax benefits on business loan EMIs?

Yes, both principal and interest components of business loans may qualify for tax deductions under relevant sections of the Income Tax Act.

Can I close my business loan before the tenure ends?

Yes, most lenders allow foreclosure of business loans, though pre-closure charges may apply. Always check your lender’s policy before deciding.

Does the EMI remain fixed for the entire loan tenure?

For fixed-rate loans, the EMI remains constant. For floating-rate loans, EMIs may vary depending on changes in the interest rate

Can I get different EMI options from my lender?

Yes, some lenders provide step-up or step-down EMIs to align with your business cash flow.

How can I reduce my EMI without extending the loan tenure?

Making part-prepayments reduces the outstanding principal, which in turn lowers your EMI without increasing the loan tenure