Understanding what is Input Tax Credit (ITC) is crucial for businesses navigating the Goods and Services Tax (GST) framework. ITC allows taxpayers to claim credit for the GST paid on purchases, which can be offset against GST liability on sales. However, not all ITC claims are permissible under GST law.

Ineligible input tax credit in the GST law determines the tax amount that a business cannot claim as a credit against the GST payable on its outward supplies. This impacts the overall tax liability and compliance requirements.

Table of Contents

What Are the Consequences of Claiming Ineligible ITC?

Claiming ineligible ITC can lead to significant consequences, including tax adjustments, penalties, and interest charges. These repercussions can affect your business’s financial health and compliance status.

What Are the Most Common Categories of Ineligible ITC?

The major categories of ineligible ITC as per Section 17(5) of the Central Goods and Services Tax (CGST) Act are listed below:

|

Category |

Ineligible ITC |

|

Motor vehicles and conveyances |

Vehicles with seating capacity ≤13 persons, except for specific exceptions |

|

Food and beverages, club membership |

Includes outdoor catering, beauty treatments, health services, rent-a-cab, etc. |

|

General insurance, servicing, repair, maintenance |

Related to motor vehicles, vessels, or aircraft, except for specific exceptions |

|

Sale of membership in clubs, health, and fitness centers |

Membership fees for clubs, gyms, etc. |

|

Renting motor vehicles, life insurance, health insurance |

Except when mandated by the government or part of a mixed/composite supply |

|

Travel benefits to employees |

Leave travel, home travel concession, etc. |

|

Works contract services |

Construction of immovable property, except for plant and machinery |

|

Construction of immovable property |

On one’s own account, except for plant and machinery |

|

Goods/services for personal use |

Goods or services used for non-business purposes |

|

Goods lost, stolen, destroyed, written off, or free samples |

No ITC is available for such goods |

|

Fraud cases |

ITC denied for tax payments related to fraud, misstatements, or suppression of facts |

|

Standalone restaurants |

Restaurants charge 5% GST but cannot avail ITC on inputs |

List of Ineligible ITC Under GST: Category-Wise

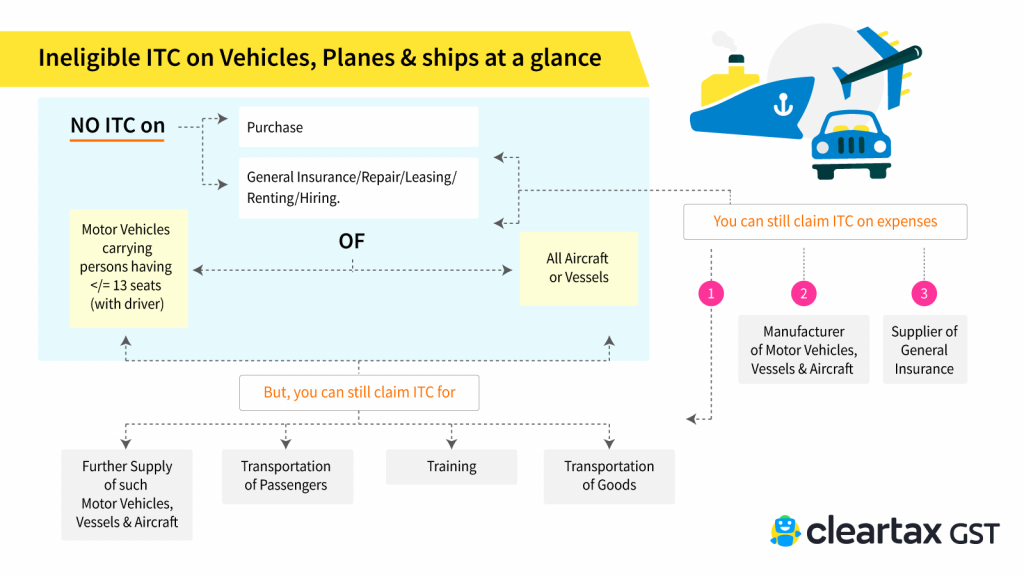

1) Motor Vehicles & Conveyances

Under GST regulations, ITC is not available for motor vehicles with a seating capacity of 13 or fewer persons, including the driver. However, an exception is made for vehicles with a seating capacity exceeding 13 people, where ITC is allowed. Additionally, ITC is not available for vessels and aircraft.

For example, if ABC & Co. purchases a car with a seating capacity of 12, they cannot claim ITC for this purchase.

Exceptions to ITC on Motor Vehicles / Vessels / Aircraft

1. Supply of other vehicles or conveyances, vessels, or aircraft

ITC is permitted if the vehicle, vessel, or aircraft is used to make taxable supplies of other vehicles, conveyances, vessels, or aircraft.

A practical illustration of this scenario is a car dealership that can claim ITC on vehicles purchased for resale or demonstration purposes to potential customers.

By allowing ITC in these cases, the GST law recognises the legitimacy of using transportation assets as direct inputs for making taxable supplies within the same industry or domain. This provision aims to prevent cascading taxation and ensure a fair tax burden for businesses operating in transportation-related sectors.

2. Transportation of passengers

ITC is allowed if motor vehicles are used for the transportation of passengers.

A practical example is a tour operator who can claim ITC on buses employed for ferrying passengers on sightseeing tours or other travel-related activities.

By permitting ITC in such cases, the GST law aims to alleviate the tax burden on businesses operating in the transportation industry, where vehicles are essential assets for rendering taxable services.

3. Imparting training on driving, flying, and navigating such vehicles or conveyances or vessels or aircraft, respectively

When vehicles, vessels, or aircraft are utilised for imparting training on driving, flying, navigating, or other related activities, ITC is permitted under GST.

A driving school, for instance, can claim ITC on vehicles employed for providing hands-on training to aspiring drivers.

By allowing ITC in such scenarios, the GST law recognises the role of transportation assets in facilitating skill development and capacity building within relevant industries. This provision ensures that businesses engaged in imparting training related to the operation of vehicles, vessels, or aircraft are not unfairly burdened with the tax incurred on their essential training assets.

4. Transportation of goods

ITC is permitted on motor vehicles used for transporting goods, with the exception of Goods Transport Agencies.

For instance, a manufacturer can claim ITC on trucks utilised for transporting their finished products to customers, recognising the legitimate business use of such vehicles.

Here’s a quick view of the ineligible ITC on motor vehicles, vessels, and aircraft:

2) Food, Beverages, Club Memberships, and Others

ITC is generally not permitted on the supply of food and beverages. However, exceptions exist for mixed or composite supplies, where ITC can be claimed if the inward and outward supply categories align. Understanding and correctly applying this exception is crucial for businesses to ensure accurate ITC claims.

For instance, if an office organises a party and provides food and beverages, ITC cannot be claimed on the expenses related to these items, as they fall under the restricted category. However, if a restaurant supplies a mixed or composite package involving both food and beverages alongside eligible services, ITC may be permissible on the entire package due to the exception. Businesses must carefully evaluate each supply to determine ITC eligibility based on the specific nature and composition of the goods and services involved.

3) Services of General Insurance, Servicing, Repair and Maintenance

GST Input Tax Credit utilisation is not permitted on services related to general insurance, servicing, repair, and maintenance concerning motor vehicles, vessels, or aircraft. This provision aims to align with the broader restrictions on ITC for motor vehicles, vessels, and aircraft themselves, ensuring consistency in the tax treatment of related services.

Exceptions to ITC on Insurance, Repair or Maintenance

The exceptions for ITC on insurance, repair, or maintenance services mirror those for motor vehicles, vessels, and aircraft. ITC is allowed when these services are used for making taxable supplies, transportation of passengers, or imparting training. Additionally, ITC is permissible when these services are mandated by law or relate to the transportation of goods.

4) Sale of Membership in a Club or Health / Fitness Centre

ITC is not allowed on membership fees for clubs, gyms, or fitness centers. For instance, if a company pays for an employee’s gym membership, it cannot claim ITC on this expense. This restriction ensures that personal and leisure expenses are not offset against business tax liabilities.

5) Rent-a-Cab, Life Insurance and Health Insurance

Input Tax Credit is generally not permissible for expenses related to rent-a-cab, health insurance, and life insurance. However, exceptions exist where ITC is allowed if the Indian Government mandates employers to provide certain services to employees, such as mandatory cab services for female staff during night shifts.

For instance, if XYZ Ltd. provides rent-a-cab services as mandated by the government, they can claim ITC for the GST paid on these services. Additionally, ITC is allowed if the inward and outward supplies fall under the same category or if they are part of a mixed or composite supply. If ABC Travels lends a car to DEF Travels, DEF Travels can claim ITC on the GST charged by ABC Travels.

ITC is also available for these services under exceptions similar to the government obligation scenario mentioned above.

6) Travel

Under GST law, ITC is not available for travel benefits extended to employees for vacations, such as leave or home travel concessions. For instance, if ABC Ltd. offers a travel package to its employees for personal holidays, the company cannot claim ITC on the GST paid for this package. However, ITC is permissible for travel expenses related to business purposes, such as attending conferences or client meetings. Understanding these distinctions is vital for accurate GST compliance. ITC is available when the employer has to provide these benefits mandatorily to the employees.

7) Work Contract

When dealing with work contract services, ITC shall not be available for any work contract services provided for the construction of immovable property, except when the input service is used for further work contract services.

Consider the following example: XYZ Contractors is constructing an immovable property. In this case, XYZ cannot claim ITC. However, if XYZ hires ABC Contractors to handle a portion of the works contract, ITC can be claimed on the GST charged by ABC Contractors. This distinction is vital for understanding eligible and ineligible input tax credit under GST.

8) Constructing an Immovable Property on Own Account

When constructing an immovable property on your own account, you should be aware that no input tax credit is available for the goods and services used in this process. This means that expenses incurred for building structures such as office buildings do not qualify for ITC under GST. However, this restriction does not apply to plants or machinery.

For instance, Ajay Steel Industries constructing an office building would not be eligible for ITC, but constructing a blast furnace for steel manufacturing would be eligible for ITC. While ITC is not available for the construction of immovable property on one’s own account, it is available for inputs used in manufacturing plants and machinery for personal use.

Composition Scheme

If you are a business owner operating under the composition scheme in GST, then you are ineligible for input tax credit. The composition scheme simplifies tax compliance but does not allow ITC claims. Ensure you explore your eligibility for the composition scheme.

No ITC for Non-Residents

Non-resident taxable persons are ineligible to claim input tax credit on goods or services received. ITC applies exclusively to goods imported by non-resident taxable persons.

No ITC for Personal Use

Under GST regulations, the goods or services used for personal purposes are ineligible for input tax credit. It’s crucial to distinguish between business and personal use to ensure compliance and avoid penalties. This rule aims to ensure that GST input tax credit eligibility strictly pertains to business-related expenses.

When inputs serve both business and personal purposes, you must calculate the common credit applicable solely to business use. This involves determining the proportion of inputs used for business and claiming ITC accordingly.

Free Samples and Destroyed Goods

ITC is not available for goods that are lost, stolen, destroyed, written off, or given as gifts or free samples. Businesses must account for such scenarios in their records, acknowledging the ineligibility of ITC on these items. Understanding these implications helps maintain accurate financial records and avoids improper ITC claims.

No ITC in Fraud Cases

ITC cannot be claimed for tax payments associated with fraudulent cases, such as non or short-tax payments, excessive refunds, or misutilisation of ITC. Fraud cases encompass willful misstatements, suppression of facts, or the confiscation and seizure of goods.

To safeguard your business, exercise caution and ensure all claims are accurate and truthful. Avoiding fraudulent practices helps maintain compliance and prevents severe penalties under GST regulations.

No ITC on Restaurants

According to Notification No. 46/2017-Central Tax (Rate), dated 14th November 2017, standalone restaurants charge only 5% GST but cannot avail ITC on inputs. For example, McDonald’s applies a 5% GST rate without ITC, while Taj’s Grill by the Pool restaurant, part of a hotel, charges 18% GST with ITC. This distinction is crucial for restaurant owners to understand the ITC rules under GST and manage their pricing strategies accordingly.

How to Identify Ineligible ITC?

Identifying ineligible ITC involves diligent record-keeping and awareness of GST regulations. Keep thorough records of all transactions and regularly review them to spot instances where ITC might be ineligible. Familiarise yourself with the list of ineligible ITCs under GST and ensure all ITC claims comply with GST laws. This practice helps avoid claiming ineligible ITC and maintains the accuracy of your financial statements.

Related Read: ITC Reversal under GST Explained

Conclusion

Understanding eligible and ineligible input tax credit under GST is important for maintaining compliance and avoiding penalties. Properly managing ITC claims ensures that your business remains on the right side of GST regulations, enhancing financial accuracy and operational efficiency.

Frequently Asked Questions (FAQs)

1. What’s the difference between ineligible ITC and blocked credit under GST?

Ineligible ITC refers to situations where the law explicitly restricts or denies the ability to claim ITC, even if GST has been paid on the inputs. Blocked credit, on the other hand, refers to the portion of ITC that cannot be utilised due to certain restrictions imposed by the GST law, such as the reversal of ITC on exempt supplies.

2. How do I record an ineligible ITC?

Ineligible ITC should be recorded separately from eligible ITC in your books of accounts. It’s advisable to maintain a separate ledger or account to track ineligible ITC and ensure that it is not claimed inadvertently.

3. How can I identify if ITC is ineligible for my business?

To identify ineligible ITC, you need to thoroughly understand the nature of your purchases and the GST regulations applicable to your business. Consulting with tax professionals, referring to the GST law and relevant notifications, and regularly reviewing your purchases can help identify instances where ITC may be ineligible.

4. Can I claim ITC on purchases for personal use?

No, ITC is not available for goods or services used for personal purposes. Only purchases made for business purposes are eligible for ITC under GST.

5. Can I claim ITC on travel expenses for employees?

ITC is not available for travel benefits extended to employees for personal purposes, such as leave or home travel concessions. However, ITC is allowed for travel related to business purposes, such as client meetings or business conferences.

6. Are there any exceptions to claiming ITC on commonly ineligible categories?

Yes, there are exceptions to claiming ITC on certain commonly ineligible categories, such as motor vehicles, vessels, or aircraft used for specific purposes like transportation of passengers, imparting training, or transportation of goods (except for Goods Transport Agencies).

7. How can I maintain proper records to avoid claiming ineligible ITC?

To avoid claiming ineligible ITC, it is essential to maintain separate ledgers or accounts for ineligible ITC, regularly review purchases, and seek professional advice or clarification from relevant authorities in case of ambiguity.

8. What is the difference between ITC reversed and ineligible ITC?

ITC reversed refers to the portion of ITC that was initially claimed but needs to be reversed or paid back due to certain circumstances, such as the ITC reversal in GST on exempt supplies or the reversal of ITC on inputs used for non-business purposes. Ineligible ITC, on the other hand, refers to situations where ITC was never eligible to be claimed in the first place, as per the GST law.