Budgeting helps you decide where your money should go, so you can meet your needs and goals without overspending. It’s a roadmap for your finances to make sure you use your money wisely.

Budgets help people and business save and spend wisely. Whether you’re an individual who wants to save money for a big purchase, or a business founder who wants to improve cash flow, a budget is a fix-all solution.

Anybody can budget – and everyone who handles money should know how to budget. In this blog, we show you what a budget is, and

What is Budgeting?

Budgeting is the process of creating a detailed plan documenting expenses and incomes over a period of time. It helps with allocating money correctly to cover expenses and meet your goals.

A budget serves as a financial blueprint, helping individuals and organisations track their financial activities and make strategic financial decisions. Let’s understand how a budget works, before diving into actually making a budget.

Understanding Budget

Making a budget is quite straightforward – you don’t need to be an accounting whiz or a math maverick to make a budget.

There are three possible outcomes to a budget – a balanced budget, surplus, or a deficit.

| Balanced Budget | Revenue = Expenses |

| Deficit Budget | Revenue < Expenses |

| Surplus Budget | Revenue > Expenses |

A budget is a microeconomic principle that illustrates the exchange and trade-offs involved when one good is swapped for another. In relation to the overall outcome of this exchange, a surplus budget indicates the anticipation of profits, a balanced budget suggests an expectation of revenues equaling expenses, while a deficit budget implies that expenses will surpass revenues.

How to Budget in 10 Steps?

Creating a budget involves a systematic approach to managing your finances effectively. Here are 10 steps to help you budget:

- Set Financial Goals: Identify your short-term and long-term financial objectives. Determine what you want to achieve, such as saving for a vacation, paying off debt, or building an emergency fund.

- Calculate Your Income: Determine your total income from all sources. Include your salary, investments, rental income, or any other sources of income. It’s crucial to have an accurate understanding of your available funds.

- Track Your Expenses: Keep track of all your expenses over a specific period, ideally a month. Categorize your expenses into fixed (e.g., rent, utilities) and variable (e.g., groceries, entertainment) expenses. Use receipts, bank statements, or apps to help you track your spending.

- Analyze Your Spending: Review your expenses to identify any unnecessary or excessive spending. Look for areas where you can cut back or make adjustments to align your spending with your financial goals.

- Create Categories: Group your expenses into categories such as housing, transportation, food, debt payments, entertainment, and savings. This will provide structure to your budget.

- Allocate Funds: Assign a specific portion of your income to each expense category. Start with essential expenses like housing, utilities, and debt payments. Then allocate funds for savings and discretionary expenses based on your financial goals and priorities.

- Monitor and Adjust: Regularly track your income and expenses throughout the period. Update your budget as necessary and make adjustments to ensure your spending remains within the allocated amounts.

- Plan for Savings: Prioritize saving a portion of your income. Aim to save at least 10-20% of your income for emergencies, future goals, and retirement. Automate your savings by setting up automatic transfers to a savings account.

- Be Realistic: Ensure that your budget is realistic and sustainable. Don’t underestimate expenses or overestimate income. Be honest with yourself about your spending habits and make adjustments accordingly.

- Review and Reflect: Periodically review your budget to evaluate your progress. Assess how well you’re sticking to your budget and achieving your financial goals. Use this review as an opportunity to learn and make improvements to your strategy.

Corporate BudgetCorporate budgets refer to the financial plans and allocations made by businesses or organizations to guide their spending, revenue generation, and overall financial management. Here are key aspects and considerations when it comes to corporate budgets:

- Revenue Projections: Corporate budgets begin with forecasting revenue projections. This involves estimating sales, analyzing market trends, considering pricing strategies, and assessing other factors that can impact the company’s income.

- Expense Categories: Businesses categorize expenses into various categories, such as operational expenses (rent, utilities, salaries), marketing and advertising, research and development, production costs, raw materials, equipment purchases, and more. These categories help allocate resources effectively and track spending.

- Fixed and Variable Expenses: Similar to personal budgets, corporate budgets distinguish between fixed and variable expenses. Fixed expenses are those that remain relatively stable, such as rent or lease agreements. Variable expenses fluctuate based on business activities, like marketing campaigns or inventory purchases.

- Capital Expenditures: Corporate budgets often include provisions for capital expenditures. These are investments in long-term assets like property, equipment, or technology upgrades that can enhance operational efficiency, expand capacity, or drive growth. Capital expenditures are typically planned over an extended period, and budgeting ensures the proper allocation of funds for these investments.

- Cost Control Measures: Budgeting enables businesses to implement cost control measures. By analyzing historical data, identifying cost drivers, and setting expense targets, organizations can implement strategies to optimize spending, negotiate better deals with suppliers, eliminate unnecessary expenses, and improve profitability.

- Cash Flow Management: Budgeting helps businesses manage cash flow effectively. By projecting cash inflows and outflows, companies can anticipate periods of cash surplus or shortage. This enables them to take proactive measures such as adjusting payment terms, managing inventory levels, or securing additional funding if needed.

- Performance Evaluation: Corporate budgets provide a benchmark for evaluating performance. By comparing actual financial results against budgeted targets, businesses can identify areas of success or potential issues. This information helps management make informed decisions, implement corrective actions, and adjust strategies to align with financial goals.

- Flexibility and Adaptability: Corporate budgets should be flexible to accommodate changes in business conditions, market dynamics, or unexpected events. Regular monitoring and periodic reviews allow for adjustments to the budget as needed. This flexibility enables organizations to respond to opportunities and challenges effectively.

- Long-Term Planning: Budgeting also plays a vital role in long-term planning and goal setting for businesses. It helps set financial objectives, determine investment priorities, and align resources to achieve strategic milestones. It serves as a roadmap for the organization’s financial journey.

- Collaboration and Accountability: Budgeting involves collaboration across various departments and teams within the organization. It fosters communication, promotes transparency, and ensures that all stakeholders understand their roles and responsibilities in achieving financial targets. It also establishes accountability for financial outcomes.

Personal BudgetA personal budget is a financial plan that helps individuals manage their income, expenses, and savings to achieve their financial goals. It provides a framework for tracking and controlling spending, making informed financial decisions, and saving for the future. Here are the key components of a personal budget:

- Income: Start by determining your total monthly income. This includes your salary, wages, freelance earnings, rental income, or any other sources of income.

- Fixed Expenses: Identify your fixed expenses, which are recurring and relatively consistent month to month. These typically include rent or mortgage payments, utilities (electricity, water, gas), insurance premiums, loan payments, and subscriptions (internet, streaming services).

- Variable Expenses: Track your variable expenses, which can fluctuate from month to month. These may include groceries, dining out, transportation costs, entertainment, clothing, personal care, hobbies, and other discretionary spending. It’s important to estimate these expenses based on your historical spending patterns or create spending limits for each category.

- Savings and Investments: Allocate a portion of your income for savings and investments. Establish specific savings goals, such as an emergency fund, retirement fund, or a specific purchase. Set aside a predetermined amount each month to build your savings and ensure a disciplined approach to reaching your financial objectives.

- Debt Payments: If you have outstanding debts, allocate a portion of your budget to make regular payments. This includes credit card debt, student loans, car loans, or any other debts you need to repay. Prioritize paying off high-interest debts first to minimize interest costs.

- Financial Goals: Define your short-term and long-term financial goals. These may include saving for a down payment on a house, planning a vacation, buying a car, paying off a loan, or investing in education. Set SMART (Specific, Measurable, Achievable, Relevant, Time-bound) goals and allocate funds toward them in your budget.

- Review and Adjust: Regularly review your budget to track your actual income and expenses. Compare your spending against your budgeted amounts and identify areas where you can cut back or reallocate funds. Adjust your budget as needed to ensure it remains realistic and aligned with your financial goals.

- Monitor and Control: Continuously monitor your expenses throughout the month to ensure you stay within your budget. Use financial tools, apps, or spreadsheets to track your spending. Avoid impulsive purchases and make mindful spending decisions to maintain control over your finances.

- Seek Professional Help if Needed: If you’re struggling with managing your finances or need guidance, consider seeking help from a financial advisor or counsellor. They can provide personalized advice, assist with debt management, and help you optimize your strategies.

Why is Budgeting so Important?Budgeting is important for several reasons:

- Financial Control: It provides you with a clear picture of your income and expenses, giving you better control over your financial situation. It helps you understand where your money is going, identify areas of overspending, and make necessary adjustments to ensure your expenses align with your income.

- Goal Achievement: A budget serves as a roadmap to help you achieve your financial goals. By setting specific goals and allocating funds towards them, you can track your progress and make informed decisions that align with your objectives. Whether it’s saving for a down payment, starting a business, or paying off debt, budgeting helps you prioritize and allocate resources accordingly.

- Expense Management: Budgeting helps you manage your expenses effectively. By tracking your spending habits and categorizing expenses, you gain a better understanding of your financial priorities. It allows you to identify areas where you can cut back, eliminate unnecessary expenses, and optimize your spending to make the most of your available resources.

- Debt Reduction: It is a powerful tool for managing and reducing debt. By allocating funds towards debt payments and strategically managing your expenses, you can make progress in paying off outstanding debts. A budget helps you avoid incurring further debt and supports your debt repayment strategy.

- Savings and Emergency Funds: Budgeting encourages regular savings and the creation of emergency funds. By allocating a portion of your income towards savings, you can build a financial safety net and be prepared for unexpected expenses or financial hardships. It ensures that saving becomes a consistent habit, helping you achieve your savings goals.

- Financial Awareness and Decision Making: Budgeting increases your overall financial awareness. It helps you make more informed decisions about your spending, saving, and investment choices. With a budget in place, you can evaluate the financial impact of your decisions, assess trade-offs, and make choices that align with your long-term financial well-being.

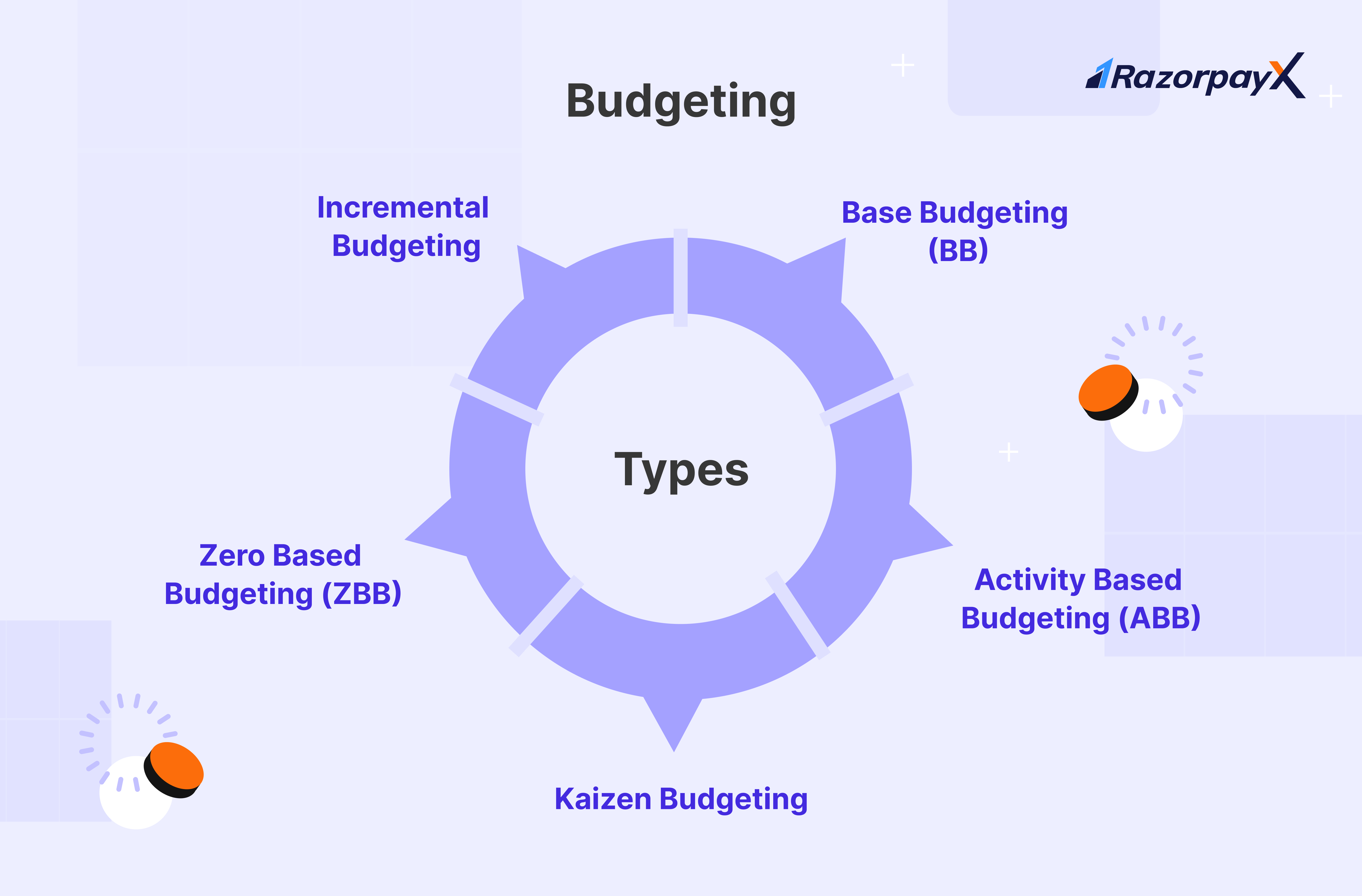

Types of Budgeting There are several types of budgeting methods that can be used depending on the specific needs and circumstances of individuals or organizations. Here are some common types of budgeting:

There are several types of budgeting methods that can be used depending on the specific needs and circumstances of individuals or organizations. Here are some common types of budgeting:

- Incremental: This approach involves making minor adjustments to the previous period’s budget. It is based on the assumption that past budgets are generally accurate and only require incremental changes. It is a straightforward method but may not allow for significant shifts in resource allocation.

- Zero-Based Budgeting (ZBB): ZBB requires starting the budgeting process from scratch, where each expense item needs to be justified, regardless of whether it was included in the previous budget. It ensures a thorough review of all expenses and encourages prioritization based on current needs and objectives.

- Activity-Based (ABB): ABB focuses on the costs associated with specific activities or tasks. It allocates resources based on the anticipated level of activity required to achieve organizational goals. This approach is particularly useful in industries where costs are directly related to specific activities, such as manufacturing or service-oriented businesses.

- Flexible Budgeting: Flexible budgets are designed to accommodate changes in activity levels or revenue. It allows for adjustments in expenses based on fluctuations in demand or other factors. Flexible budgeting is helpful when dealing with uncertain or variable conditions.

- Cash Flow Budgeting: Cash flow budgeting focuses on managing and projecting cash inflows and outflows. It helps individuals and businesses ensure they have sufficient cash to cover expenses and meet financial obligations. Cash flow budgeting is especially important for maintaining liquidity and avoiding cash shortages.

- Rolling Budgets: Rolling budgets involve continually updating and extending the budget as time progresses. It typically covers a fixed period (e.g., 12 months), and as each month or quarter is completed, an additional month or quarter is added to the budget. Rolling budgets provide a dynamic view of the financial forecast and facilitate better adaptability to changes.

- Project Budgeting: Project budgeting involves creating a budget specifically for a particular project or initiative. It estimates the costs associated with the project and allocates resources accordingly. Project budgets help in monitoring project expenses and ensuring that costs are managed within the allocated limits.

- Performance-Based: Performance-based budgeting focuses on allocating resources based on the expected outcomes or results. It requires setting specific performance targets or metrics and allocating funds based on the projected impact on achieving those targets. This approach promotes accountability and strategic resource allocation.

Example of Budgeting

Income:

- Salary: Rs 50,000 per month

Expenses:

- Rent: Rs 15,000

- Utilities (electricity, water, internet): Rs 2,000

- Groceries: Rs 10,000

- Transportation (gas, public transportation): Rs 5,000

- Health insurance: Rs 3,000

- Dining out/entertainment: Rs 4,000

- Debt payments (student loan, credit card): Rs 6,000

- Savings: Rs 10,000

- Miscellaneous (clothing, personal care): Rs 4,000

Total Expenses: Rs 59,000In this example, the person’s total expenses exceed their income by Rs 9,000. They would need to adjust their spending or find ways to increase their income to ensure their budget is balanced. They may consider reducing discretionary expenses, finding ways to save on utilities or transportation costs, or exploring opportunities for additional income through side jobs or freelance work.Ways to Budget When BrokeBudgeting, when you’re broke or facing financial challenges, can be challenging, but it’s still possible to take control of your finances and make the most of your limited resources. Here are some ways to budget when you’re broke:

- Assess Your Income and Expenses: Start by evaluating your income and expenses. Understand how much money you have coming in and where it is going. Track your spending for a month to identify areas where you can cut back or eliminate unnecessary expenses.

- Prioritize Essentials: Focus on covering your essential needs first. These include rent/mortgage, utilities, groceries, and transportation. Allocate a portion of your income to these priority expenses before considering other discretionary spending.

- Cut Back on Discretionary Expenses: Identify non-essential expenses that you can reduce or eliminate. This could include dining out, entertainment, subscriptions, or impulse purchases. Look for free or low-cost alternatives for entertainment and find ways to reduce discretionary spending to free up more money for necessities.

- Negotiate Bills and Expenses: Reach out to service providers and creditors to negotiate lower rates or payment plans. Many companies are willing to work with customers who are experiencing financial difficulties. This can help reduce the financial burden and give you more breathing room in your budget.

- Look for Ways to Increase Income: Explore opportunities to increase your income, even if it’s temporary or part-time. Consider freelance work, gig economy jobs, or utilizing your skills for side projects. Any additional income can provide some relief and help you meet your financial obligations.

- Seek Assistance Programs: Check if there are government assistance programs or local community resources available to support individuals in need. These programs can offer assistance with housing, food, healthcare, or other essential services, providing temporary relief and helping you allocate your limited resources more effectively.

- Create a Bare-Bones Budget: Create a bare-bones budget that focuses solely on covering your essential needs. Trim your expenses to the absolute minimum required for survival. While this may be a temporary measure, it can help you manage your finances during tough times and ensure you have enough to meet basic needs.

- Build an Emergency Fund: Even when money is tight, try to save small amounts whenever possible. Establish an emergency fund to handle unexpected expenses and prevent you from going further into debt. Start by setting aside any spare change or small amounts you can save regularly.

In conclusion, budgeting is a crucial tool for financial success. It helps individuals and organizations take control of their finances, prioritize their spending, and work towards their goals. By creating a budget, you can track your income and expenses, make informed decisions, and save for the future. Budgeting promotes financial discipline, reduces debt, and provides a sense of security. It empowers you to live within your means, allocate resources effectively, and make conscious choices about how you spend your money. With budgeting, you can achieve financial stability and create a solid foundation for a brighter financial future.Get RazorpayX Current Account – it’s built for disruptors like you We know managing a startup can be hard. That’s why we created a current account that is tailor-made for startups like yours. With RazorpayX Current Account, you get:

- Easy credit: Guaranteed collateral free Credit Cards

- Powerful automation: Taxes, Vendor Payments, Payroll and more.

- Smart Dashboard: Manage inflows and outflows seamlessly

- Forex Services and more

- Integrated access: Access via desktop, mobile or your smartwatch.

Sign up for RazorpayX powered Current AccountFrequently Asked Questions