I believe it was the summer of ’99 when I was intrigued about the contents inside a maroon-coloured envelope that my father had bought while returning from work. The colour as well as the size definitely caught my eye and as a kid who wants to unwrap gifts or presents, I asked him if I could open and see what’s inside. My father had told me it was something important that he didn’t know much about, so he first wanted to open it and read through. Inside the envelope, there were a few booklets, some papers, and a rectangular-shaped plastic thing – all of which had UTI Bank (now Axis Bank) mentioned on them.

Later, when my father told me that he could not only check his bank balance but also take out money from a machine using that rectangular plastic thing, my curiosity as well as excitement knew no bounds! That was my first introduction to transactional cards. Little did I know then that I would sometime in life be working in the banking & finance industry, a part of which has been glorified as fintech by the startup ecosystem.

From then to now, the industry has seen a transition from magnetic strips to chip cards to recently, contactless cards. Transactional cards have not just evolved in terms of providing better security but also eased payment options for the consumers. Before we explore the components of a credit card, let us first go through the history of how it all started.

The theory

The concept of transactional cards can be found in history as far as 1890 in the novel Looking Backward by Edward Bellamy, where the term credit card has been mentioned eleven times. It is cited as a card that can be used for purchasing goods by spending a citizen’s dividend from the government, rather than borrowing.

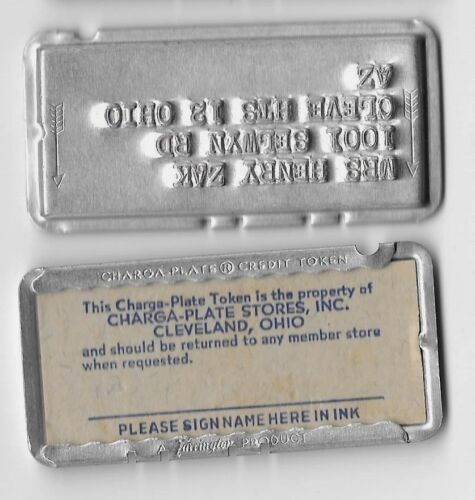

First offering – Card by businesses for their individual store

Charga-Plates are considered to be the first stepping stone in the history of transactional cards.

It came into existence in 1928 in the US and was offered by merchants to their regular customers. These plates were specific to individual stores and could only be used in those stores. Manual entries were maintained whenever a user made any purchase.

First card by a bank

The National Bank of Brooklyn in New York was the first bank to issue a charge card in 1946. They released the “Charge-It” program between bank customers and local businesses. The businesses had to deposit their sales slips to the bank, which in turn were used to bill their customers.

First card across multiple business stores

Diners Club further introduced the Diners Charge Card in 1950, providing the facility to shop at several stores with the same card. Customers were sent a monthly statement of their expenses, which they were then required to pay. Businesses were required to pay a service charge to the credit card issuer in the range of 3–5 percent of the total sales value. This was by far the closest offering that one can corelate to the card transactions that happen these days.

First interbank card

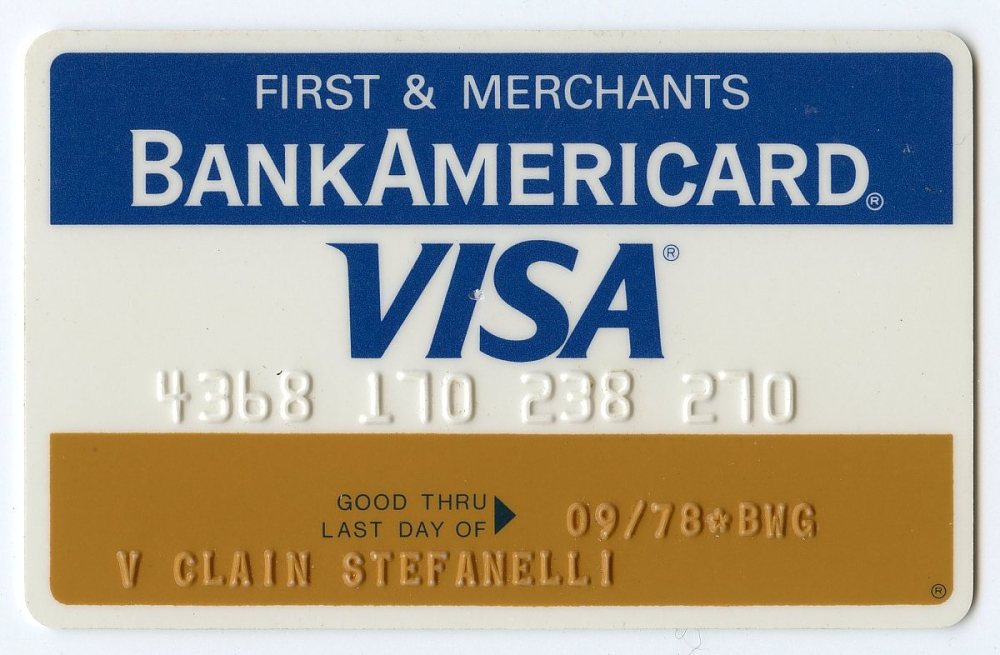

Bank of America issued the BankAmericard credit card later in 1958, which was renamed to Visa in 1976 when it collaborated with other banks who wanted to offer card services without having to build the entire system themselves. VISA stands for Visa International Service Association.

Competition between interbank cards

In 1979, the Mastercard brand came into existence, which was formerly called the Interbank Card Association and Master Charge.

And finally International cards

Both VISA and MasterCard set up ground rules and policies around issuing, usage, payments, etc on cards of different banks worldwide. What we are seeing today is, in my opinion, broadly a work of these two companies that have facilitated merchants to now accept payments not just from the same city or state or country but also internationally! As of today, MasterCard controls 25% of the global payments whereas Visa stands ahead with 61.5% of the payments market share.

Fun Fact: Diners Card was the first company to introduce cards in India. This was initiated by Mr. Kali Mody in 1961.

Credit cards in India

In the 1960s, people who lived or traveled to foreign countries were the only ones who opted for the Diners Card offerings in India. The adoption towards credit cards was so slow that it took 15 years to reach 8,000 Diners Card registered users in India.

The Central Bank of India launched the first bank credit card in 1980, which was followed by Andhra Bank in the same year – both were of the Visa brand. MasterCard was introduced to Indian consumers by Vijaya Bank in 1988. The key differentiator then was that Vijaya Bank allowed customers to withdraw cash from their branches. The eligibility of getting a credit card was entirely based upon the income of the consumers.

Between 1988 to 1993, a lot of PSU banks started issuing credit cards to their customers. At the same time, ATMs also started increasing in India. Seeing this as an opportunity, Indian banks started issuing debit cards to their customers, providing the convenience to withdraw money from their account whenever they wanted to from an ATM machine. This is how debit cards got their name as “ATM Cards.”

The credit card industry started gaining popularity due to wider acceptability at shops and better product offerings in a competitive landscape. These days, banks offer bundled insurance benefits, zero liability in terms of frauds, reward point systems, etc as well.

Fun Fact: ATM stands for Automated Teller Machine and NOT Any Time Money as people like to believe.

By the late 1990s, a significant number of consumers in the Indian market were aware of credit card and debit card products. The next big thing to start in India was online payments – only limited by internet penetration and card availability. Post the launch of players like IRCTC (2002), MakeMyTrip (2005), and Flipkart (2007) people started availing online services not just via internet banking services of their bank account but also cards.

By 2010, credit and debit cardholders had started making payments online and availing services very frequently. The next decade was the key turning point for the Indian digital payment systems.

Rupay was launched by the National Payment Council of India (NPCI) in 2012 with the vision of issuing Indian brand debit, credit and prepaid cards. By 2018, Rupay started gaining traction in tier 2 and tier 3 cities, and today, Rupay Debit Cards have higher penetration in India than Visa and MasterCard.

Understanding the cards you use

The card industry and card-issuing banks have evolved over the years with a goal to ensure transactional security as well as provide ease of shopping for their customers. Being a cardholder, it is your responsibility to know about card features and elements very well to avoid card-related fraud.

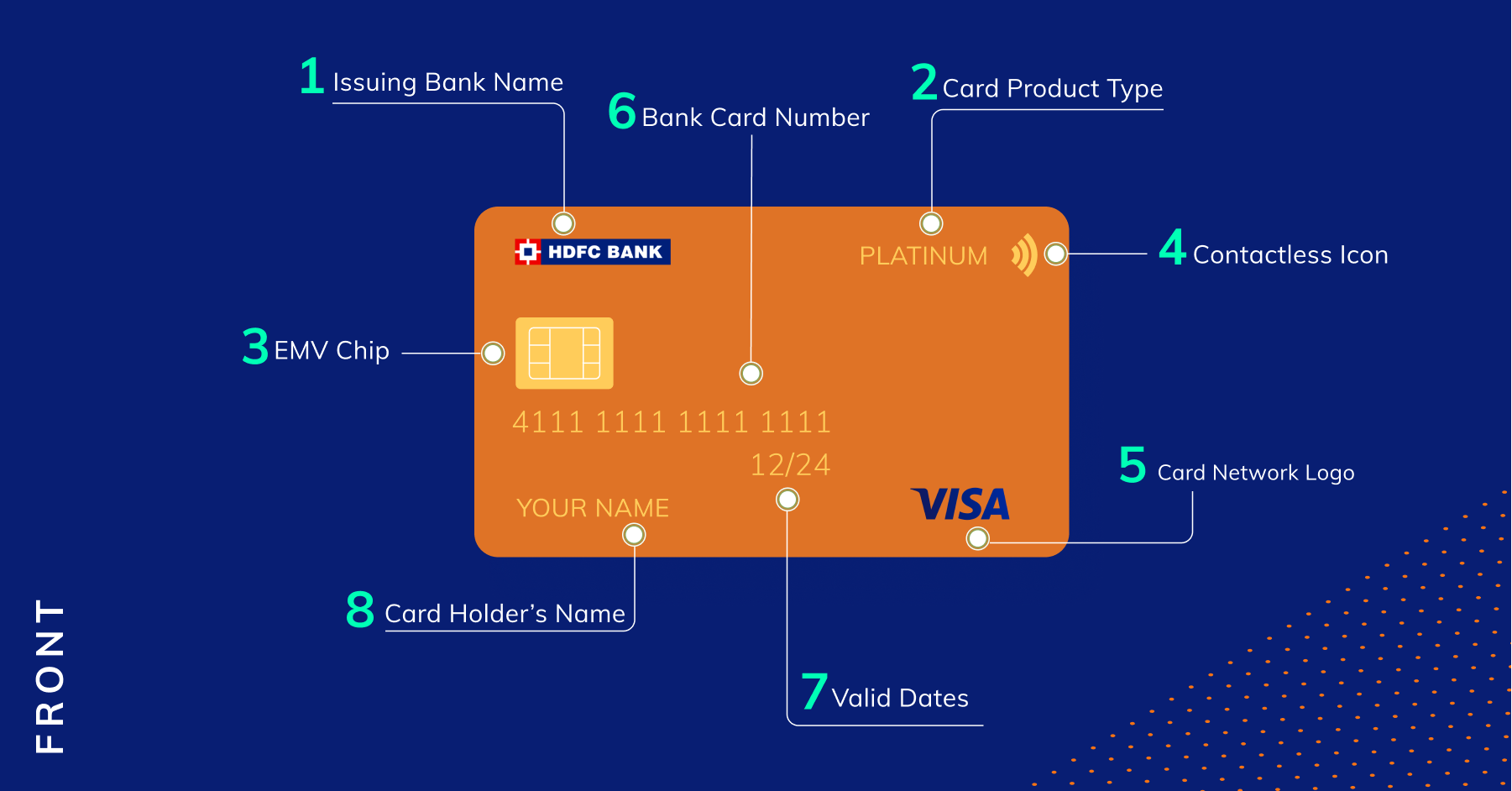

If you notice, there are various elements on your credit card and debit card. Have you ever wondered what is their purpose and significance for making online or offline payments? Let’s take a look at the front side of the card, which is the fanciest shiny face of the card.

- Issuing bank name or logo – The logo of the bank that has provided you the debit/credit card. Few banks just print their name instead of adding their logo. This can be found in the top right or left corner of the card

- Card product type – Every card will have their product name, e.g. Platinum, Titanium, Jet Privilege, etc. Every card product has features and offerings defined by their banks. You should definitely read the most important terms and conditions (MITC) at least once in your lifetime to understand annual fees, late payment charges, etc that vary per card

- EMV chip – Newly generated credit and debit cards in India have a metal square chip on the front side of the card, which stores sensitive data and provides better security as compared to the traditional magnetic strip that is found on the backside of the card. EMV chips are also used by the POS machine and the ATM machine to perform transactions. EMV chips are difficult to clone and hence, fraud related to cloning of comparatively a magnetic strip card is relatively low

- Contactless icon – You might notice a wifi or wave type of symbol on top of your card – that’s the icon of the contactless feature of a card. You can pay on a POS machine without even entering the PIN. This works only when the amount is less than Rs. 2000 and the machine also has this wifi or wave symbol. If the total amount is above Rs. 2000 then you would be asked to enter the PIN. The purpose of this feature is so you don’t have to handover cards to anyone and it would work by just tapping on the machine. Contactless payments offer the same level of security as a chip card

- Card network logo – Often called ‘card brands’ or ‘card schemes,’ these are companies that connect the issuing bank and acquiring bank to facilitate an online payment. Rupay, Visa, MasterCard or Amex are examples of this.

Related Read: What are POS Machine Charges and Transaction Fees?

Fun Fact: Did you know that the very first digit of your card represents the card network? Number 3 is for Amex, 4 is for Visa, 5 is for Mastercard, 6 is for Rupay. Go ahead and verify this against your cards!

- Card number – These 14 to 19 digit card numbers are the most sensitive element of your card. The number that you use to make online purchases – a unique series of digits which are mentioned on the top of the card. It identifies your account with the card-issuing bank. Card numbers shouldn’t be shared with anyone. Online frauds are possible if someone is aware of your card number, expiry date. Card numbers vary in length as per the issuing bank. You would be surprised to know that these are not just unique 16 digit numbers but there is a logic to generate the card number.

-

-

-

-

-

-

-

- First 6 digits: Bank Identification Number(BIN) – every bank in the world will be issued with a 6-digit number by card networks (Visa/MasterCard), which is used to identify the issuer of the card. By just looking at the first 6 digits of your card, one can know the card network and issuing bank of your card.

- Digits 7 – 15: Primary Account Number (PAN), which is uniquely assigned by the bank to every cardholder to identify them. This is very critical information and that’s why you must have seen that these are masked in most bank account statements.

- Digit 16 – Often called a check digit that is determined mathematically by a formula called the Luhn Algorithm. This digit is derived by applying the Luhn Algorithm on the previous 15 digits of the card. That’s why you might have noticed whenever you enter a wrong card number during online checkout, it will immediately highlight that the card number is incorrect as the system performs a check based upon the Luhn Algorithm.

-

-

-

-

-

-

-

- Validity dates: Few cards have both the issuing date and expiry date, but some cards will have just the expiry date. This is mostly used to shop online and also to know the validity of your card. In case your card is about to expire, the bank will automatically send you the new card to your mailing address before your card expiry date. That’s why it’s always said to have your postal address updated with your bank.

- Cardholder name – Your name is embossed on the card to provide you the feel of having a personalized prized possession. If your card was issued as part of your instant account opening process, then your name won’t be available. You can always reach out to your bank to reissue the card with your name on it.

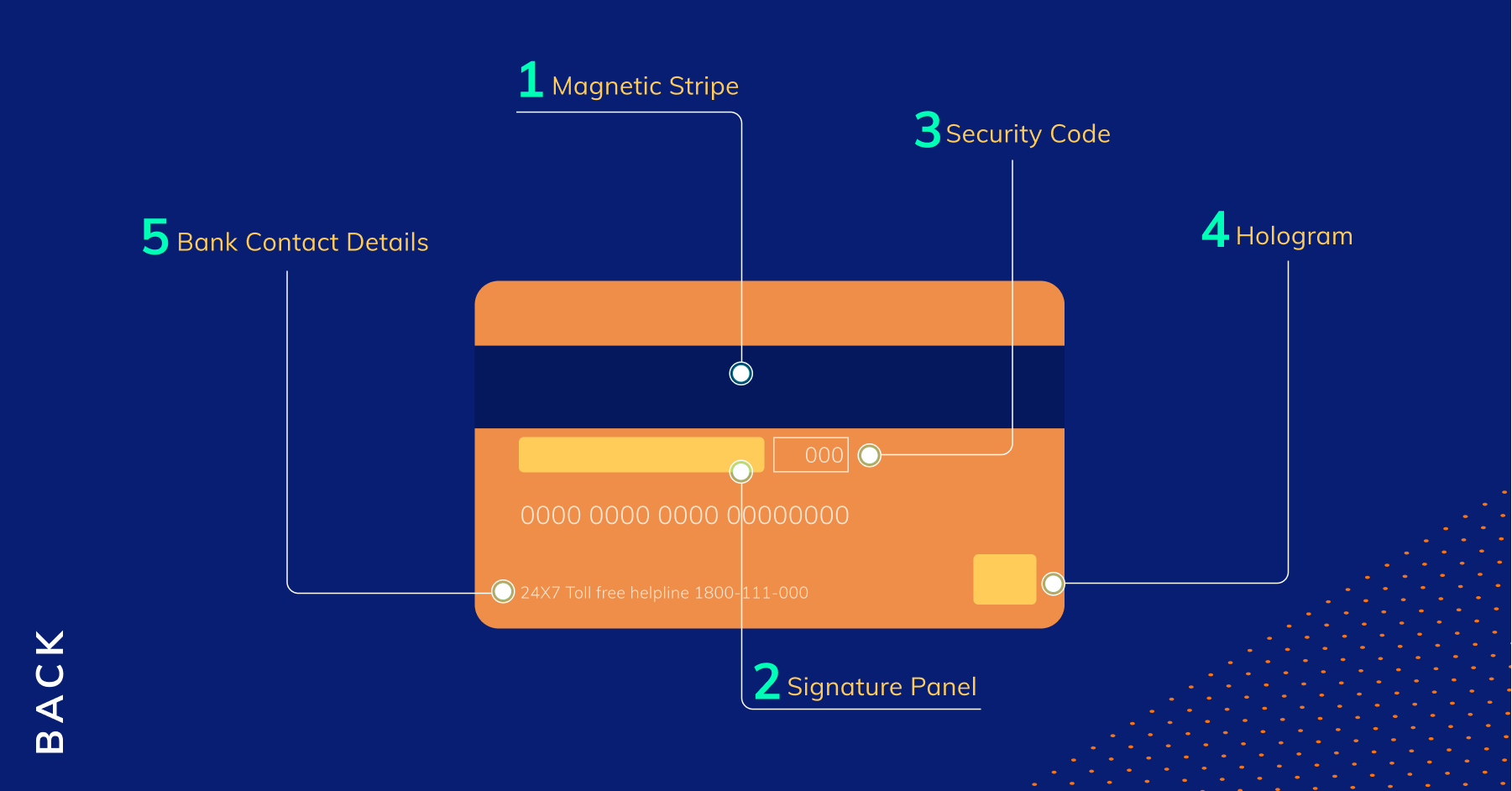

The reverse side of the card is mostly plain, but some important information does exist that needs to be preserved by you.

- Magnetic strip: The long black or grey strip on the back of your card stores all of your card information that can be read by a specialized card reader machine, the one which you see at any shop where the cashier swipes the magnetic strip of your card to receive your payment. Magnetic strips can be cloned via a card skimming device and all your card information can be stolen to create a clone card, which can be used for frauds. If you are shopping at a physical store, always prefer to use contactless or chip-based payment methods rather than swiping the magnetic strip

- Signature panel: The most ignored feature of the card by a cardholder! Whenever there is a suspicious transaction, businesses can always match the signature on the card with the actual signature the person is able to do. It is very important that as soon as you get your new card you should sign on your card in the signature panel. Also, this feature is kind of deprecated now by the use of PINs

- Security code: Also referred to as CVV, CVC, CVV2, CID, CVC, or CSC. The purpose of this security code is to provide additional security to shop online. Amex has 4 digit CID that is printed on the front side of the card whereas for MasterCard/Visa/Rupay, it is in the form of 3 digits printed on the backside of the card

- Hologram: Hologram is a way to prove that a card is valid and not a cloned one. Holograms are difficult to fake. Some of the issuers do provide holograms on the front side of the card. However, not many businesses are aware of this hologram feature and generally don’t check for this while accepting a payment

- Bank contact details: Generally, you will find contact numbers of the bank call center. These are very helpful if you need quick help or if your card is not working or you need to get it blocked. Banks also mention their address in the same place to ensure that in case the card is lost, it can be delivered to the bank’s address

In conclusion

Isn’t it amazing how a small plastic card captures so much information and functions smoothly both online and offline? What’s more interesting is how it interacts with different systems in the offline and online worlds.

This article is one of the first in the series of our effort to share the knowledge and experiences around cards. Stay tuned for more!