When UPI was first launched in 2016, it was rightly heralded as a game changer. We couldn’t agree more, because the inherent structure of the NPCI’s flagship offering is designed to become the sole platform for seamless interoperability of PSPs (Payment Service Providers) in the country.

But for it to become a truly universal payment option, the existing UPI solution needs to be more than a peer-to-peer platform. And the UPI 2.0 is just that! The upcoming launch is a much better, revamped version of UPI that will go a long way in increasing digital adoption in the business sphere, and for peer-to-merchant transactions.

UPI 2.0 – The New ‘For Merchant’ Features

We all are aware that the upgraded UPI will have many new features; such as increased transaction limit of INR 2 lakhs. However, it is the ‘for merchant’ features – the one that will directly impact P2M transactions – that are of importance.

Use of overdraft accounts

Up until now, UPI payments were made only from saving accounts. But with overdraft accounts coming into play, merchants will be able to withdraw money even when there is a cash-deficit in their account. Business, therefore, does not have to stop just because of a temporary issue of insolvency.

Capture and hold facility

The facility to block a certain amount in user’s cards was already present due to a feature called ‘key auth’. Now, merchants accepting payments via UPI will also be able to do the same. Essentially, they will be able to block a certain amount of money on their user’s cards and debit/refund it a later date.

With this feature, UPI will become useful for a variety of business verticals (where it may not have been as popular before). Hotels, e-commerce companies, cab-booking services can block amounts on their guests’ credit cards as advance. This can also be done against security.

Businesses can then refund the same once the booking is completed. This will also be of use when buying stocks or IPOs and other such transactions.

Support for invoicing

Invoices, bills, or any other supporting documentation is not a necessity when making a peer-to-peer payment. A confirmation of receipt via mail or SMS is what most businesses look for.

However, in the P2M payment space, invoices are mandatory. So far, a merchant could only add a description of the payment asked. The support for invoices in UPI 2.0 means that businesses can use a single platform for sending invoices and receiving payments, instead of using separate mediums for the same.

Easy resolution of refunds

Another reason why UPI had not permeated deeply into the business sector was that refunds were not a part of the initial core spec. So, if a merchant needed to refund money to their customer they would need to issue a fresh transaction. Now, UPI payments will also follow this mapping so that users and merchants can have clarity on the refunds made.

Related read: Types of UPI frauds and how to stay safe

How the Upgrade Will Affect the Industry?

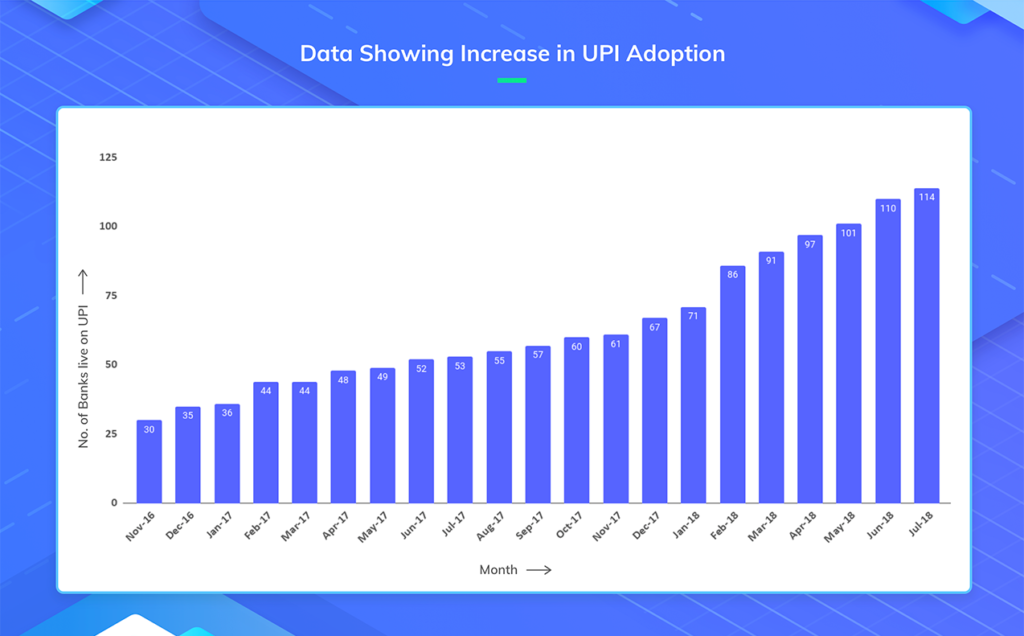

The increased popularity of UPI will also reduce the market for Wallets. Recent data shows that transactions on prepaid instruments like cards and Wallets have reduced by 14% between March 2017 and March 2018.

With UPI, this number will reduce further. Customers will want to use a platform that will allow direct bank transfer of money rather than uploading money into their Wallets.

There is no doubt that the added features will open more use cases in the business sector, and allow for greater permeation. The capture and hold feature, by itself, can create hundreds of new use cases in the e-commerce industry.

Support for invoices will convert UPI from just a transactional medium to an informational medium as well. Refund mapping will solve a crucial industry pain point which will also translate into better user experience and more transparency.

Related Read: What Is The UPI Reference Number?

What’s Missing From UPI 2.0?

As a comprehensive payment firm, Razorpay has been ready for UPI 2.0 for a while. We follow mandatory KYC procedures for all businesses, making acceptance of bank payments a breeze. We also have the industry knowledge and tech required to build on the new use cases offered by UPI.

However, there is one feature missing from the new launch, which is ‘mandates’. Mandates or standing instructions mean that UPI can become the go-to payment option for all recurring payments like SIPs, Mutual Fund payments, monthly subscriptions etc.

Also, the withdrawal of biometric Aadhaar-based payment feature will render it unusable by those who do not own a smartphone. The smartphone penetration rate in India will reach 28% by the end of 2018. This means leaving roughly 72% of the population deprived of the choice to use UPI, or any other digital payment solution.

Related Read: What is Recurring Billing? – Types, Advantages, and Examples

Looking Ahead: What the Payments Industry Needs UPI to Be

Customers always prefer simpler, ubiquitous payment solutions that can reduce friction during online transactions. UPI transactions are direct and easier; as compared to loading money into, and withdrawing from, a prepaid instrument.

UPI can easily replace PoS solutions and make accounting and reconciliation easier for merchants.

For it to become the leader in digital transactions, it has to offer ubiquity. And it must drive large-scale adoption of digital payments. NPCI also needs to build a large merchant-acceptance network; both online and offline, because that is where the real push for ‘Digital India’ will come from.

**Originally published in Inc42.