In 2026, Singapore has solidified its status as a digital by default economy. The era of physical cash is rapidly receding, replaced by a sophisticated ecosystem of mobile payment applications. According to the Monetary Authority of Singapore (MAS), digital payment adoption has reached a staggering 92%, with the market value projected to hit US$113.7 billion by the end of this year.

For a Singaporean merchant or MSME, a digital wallet is no longer just a nice to have consumer convenience. It is the critical infrastructure for conversion, security, and real-time settlement. Understanding how these wallets work is the first step toward optimizing your checkout experience and reducing cart abandonment.

Key Takeaways

- The PayNow Advantage: A single PayNow QR code allows you to accept payments from every major Singapore banking app, including DBS PayLah!, UOB TMRW, and OCBC Digital.

- Two Core Types: Wallets are either credential-based (like Apple Pay) or balance-based (like GrabPay).

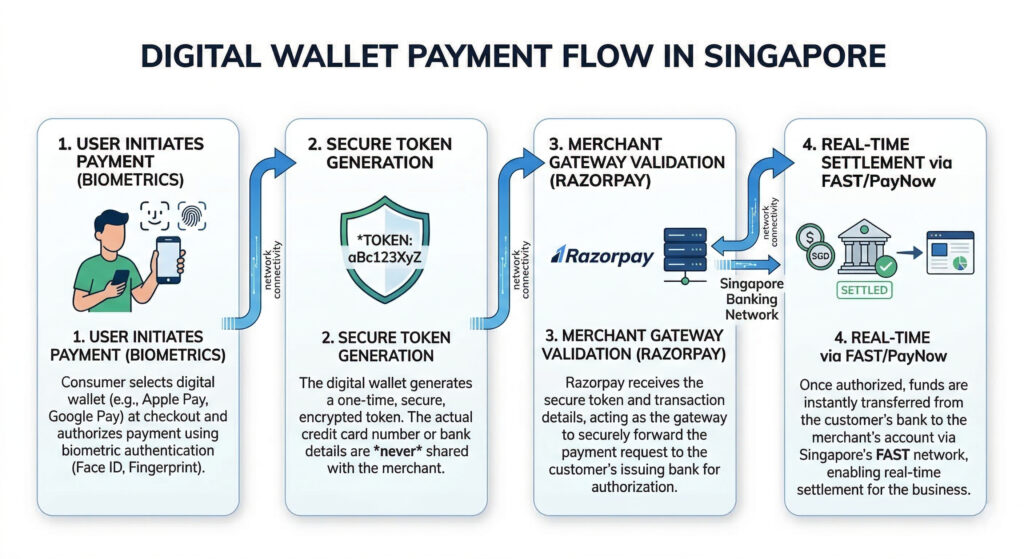

- Instant Settlement: Most local wallet transactions move via the FAST (Fast and Secure Transfers) network, ensuring immediate liquidity for businesses.

- 2026 Security Standards: New MAS mandates include 12-hour cooling-off periods for new logins and mandatory kill switches to protect against unauthorized access.

- Razorpay Integration: Platforms like Razorpay Singapore unify these fragmented methods into one simple dashboard.

What is a Digital Wallet and How Does it Work?

A digital wallet is a software-based application that securely stores payment credentials (like tokenized credit card numbers) or digital currency, allowing users to make seamless transactions.

The Transmission Technology

Digital wallets communicate with merchant terminals or gateways using two primary methods:

- NFC (Near Field Communication): This powers tap and pay transactions. When a customer holds their phone near a terminal, an encrypted signal transmits payment data instantly.

- Dynamic QR Codes: Common in e-commerce and F&B, these codes contain specific transaction data (amount and merchant ID). When scanned, the wallet initiates a direct transfer.

Credential-Based vs. Stored-Value Wallets

It is important to distinguish between how funds are accessed:

- Credential-Based (Pass-through): Wallets like Apple Pay or Google Pay do not hold money. They act as a secure conduit for a customer’s existing credit or debit cards.

- Stored-Value (Balance-based): Wallets like GrabPay or ShopeePay hold a monetary balance that users top up via bank transfers.

Singapore’s Payment Infrastructure: The Rails Powering Your Business

Behind every app is a complex set of financial pipes that move the money.

The Ubiquity of PayNow and SGQR+

PayNow is the universal connector of the Singaporean financial system. It allows users to send money using only a Mobile Number or a Unique Entity Number (UEN).

Critical for Merchants: You do not need a separate QR code for every bank. A single PayNow QR is interoperable. Whether your customer uses DBS PayLah!, OCBC Digital, or UOB TMRW, they can all scan the same code to pay you. This has been further streamlined by SGQR+, which unifies multiple payment schemes into one sticker.

Seamless Borders: Regional Linkages

Singapore has led the world in cross-border connectivity. Your PayNow QR can now accept payments from international visitors using Thailand’s PromptPay, Malaysia’s DuitNow, and India’s UPI. This is a game changer for merchants in tourist-heavy districts or those selling to regional clients.

The Leading E-Wallets in the Singapore Landscape

The market is divided into three strategic categories:

1. The Bank-Linked Giants (The PayNow Group)

These are the most common wallets. Because they are tied directly to bank accounts, they have the highest trust levels. DBS PayLah! remains a dominant force, particularly for everyday micro-transactions or student-focused rewards.

2. Ecosystems and Super Apps

Apple Pay, Google Pay, and GrabPay dominate the mobile-first demographic. Since 85% of online shoppers in Singapore are under age 44, supporting these is mandatory for conversion. GrabPay, in particular, attracts point hunters who want to earn rewards on every transaction.

3. Multi-Currency and Web3 Innovations

As a global hub, Singapore sees high usage of wallets like Revolut and YouTrip for zero-fee foreign exchange. Furthermore, MAS guidelines for Stablecoins and Cryptoassets have paved the way for crypto-linked cards (like Nexo or Crypto.com) to be used at standard merchant points of sale.

| Wallet Type | Examples | Primary Technology | Best For |

| Bank-Linked | PayLah!, OCBC Digital | PayNow QR / FAST | Low-cost, local transactions |

| Super App | GrabPay, ShopeePay | QR Code | Loyalty and rewards |

| Device-Based | Apple Pay, Google Pay | NFC | Fast, physical tap-to-pay |

| Multi-Currency | YouTrip, Revolut | Card / NFC | Travelers and FX savings |

Security and Regulation: Protecting Your Revenue

Security concerns are ever-present, with scam losses in Singapore reaching S$913 million in 2025. To combat this, the landscape is heavily regulated.

- Tokenization: Digital wallets do not share actual card numbers with you. They send a token, which is useless if intercepted by hackers.

- 3D Secure 2.0 (3DS2): This protocol is standard for Razorpay merchants. It uses biometrics and behavior analysis to verify transactions, shifting the liability for fraudulent chargebacks away from your business.

- Shared Responsibility Framework: MAS has implemented a framework that clarifies liability between banks, telcos, and consumers, ensuring a safer ecosystem for digital trade.

- Mandatory Kill Switches: In 2026, all Major Payment Institutions (MPIs) must provide a kill switch that allows users to instantly freeze their accounts if they suspect a breach.

The Future: Agentic Commerce and Biometric Passkeys

The next phase of digital wallets involves Agentic Commerce, where AI assistants can negotiate and pay for services on behalf of the user. We are also seeing a shift away from vulnerable One-Time Passwords (OTPs) toward Biometric Passkeys, which use facial recognition or fingerprints to authorize payments, making OTP interception scams a thing of the past.

The Merchant Challenge: Fragmentation and Friction

While these options are excellent for customers, they can create a logistical hurdle for MSMEs. Managing fragmented settlement reports and varying fee structures can drain vital business resources. Furthermore, in an era of heightened security, it is essential to partner with a platform that operates within the MAS regulatory framework. Choosing a partner that utilizes licensed infrastructure ensures that your business stays compliant and that every cent of your revenue is securely safeguarded.

Empowering Businesses with Razorpay Singapore

Razorpay acts as the aggregator that solves this fragmentation.

- All Banks, One Integration: By enabling PayNow through Razorpay, you automatically accept payments from every major bank app (DBS, UOB, OCBC) without multiple setups.

- Payment Links & Pages: You can accept these wallets even without a website. Create a Payment Link or Payment Page and send it via WhatsApp or email to get paid instantly.

- B2B Efficiency: Razorpay handles UEN-based collections and dynamic QR codes, which has been shown to reduce order-taking time by 10% for high-volume businesses like F&B.

Ready to Scale Your Singapore Business?

Streamline your financial operations with a unified payment platform designed for the Lion City.

Accept PayNow, cards, and digital wallets effortlessly while keeping your finances reconciled and IRAS-compliant.

Conclusion

In 2026, a merchant’s success is tied to their payment agility. While the underlying technology of NFC, FAST, and Tokenization is complex, the goal is simple: provide a frictionless, secure checkout that meets the customer where they are. Transitioning to a unified platform is the most effective way to future-proof your business in Singapore’s dynamic digital economy.

Frequently Asked Questions (FAQ)

1. Can a PayNow QR be scanned by any banking app?

Yes. A PayNow QR code is a universal standard in Singapore. It can be scanned by all major banking apps, including DBS PayLah!, OCBC Digital, and UOB TMRW, allowing for instant interbank transfers.

2. What is the difference between a digital wallet and a mobile wallet?

A digital wallet is the broader software term (accessible via desktop or mobile), while a mobile wallet is a version specifically optimized for smartphones to use NFC or QR codes for in-person payments.

3. Are digital wallets safe for merchants in Singapore?

Yes. By using 3DS2 and tokenization, digital wallets significantly reduce the risk of fraud. These technologies ensure that sensitive card data is never stored on your servers, reducing your PCI compliance burden.

4. What is SGQR+?

SGQR+ is the enhanced version of Singapore’s unified QR code. It allows a merchant to use a single QR sticker to accept a vast range of both local and international payment schemes through one single provider.

5. How long does it take for PayNow payments to settle?

Payments made via the FAST network (which powers PayNow) typically settle in real-time. This means the funds are credited to your business account almost immediately after the customer authorizes the payment.

6. Do I need a separate account for DBS PayLah! and OCBC Digital?

No. If you have PayNow enabled via a payment platform like Razorpay, you can accept payments from all bank-linked wallets through one single interface and one consolidated settlement report.